The 100 Minus Age Asset Allocation: Balance Growth and Safety with One Rule

The 100 Minus Age Asset Allocation: Balance Growth and Safety with One Rule

The 100 Minus Age Asset Allocation rule is one of the oldest and simplest principles in personal finance. It gives investors a quick way to decide how much money should be invested in equities and how much should go into safer assets such as bonds or fixed income instruments.

This rule is widely used in retirement planning and beginner investment guides because it removes complexity from decision making.

In recent years, this rule has gained renewed attention as people look for stable and disciplined ways to manage risk.

While modern strategies now focus more on personalization, the 100 Minus Age rule still serves as a practical foundation for understanding how age and risk tolerance are connected in long term investing.

Table of Contents

Key Takeaways

- The rule suggests equity allocation equals 100 minus your age.

- It helps balance growth and capital protection over time.

- Younger investors can hold more equities due to longer time horizons.

- Older investors shift more toward debt to reduce volatility.

- The rule is a starting point and should be adjusted for personal goals and risk tolerance.

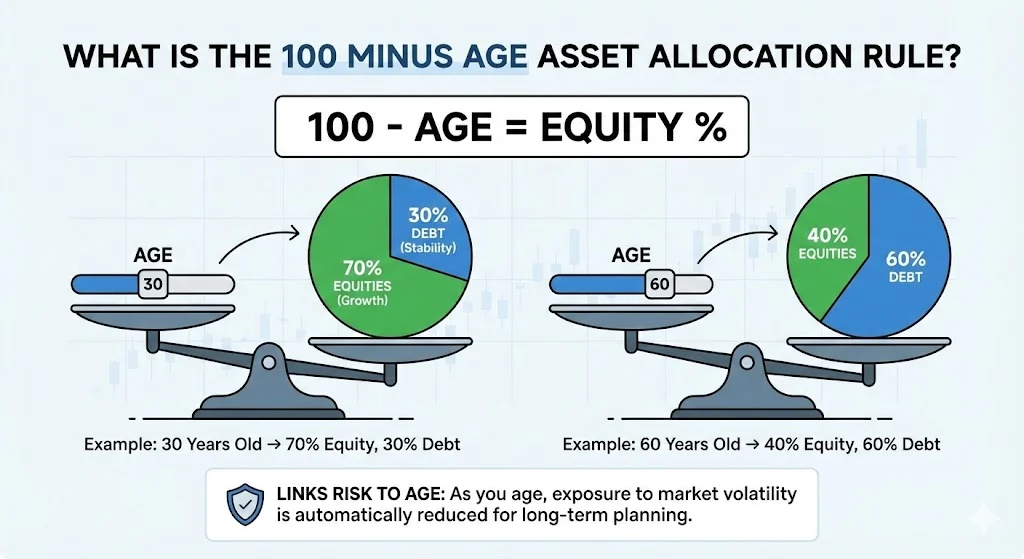

What Is the 100 Minus Age Asset Allocation Rule?

The 100 Minus Age rule is a simple formula used to guide asset allocation. It states that the percentage of your portfolio invested in equities should be equal to 100 minus your current age. The remaining portion should be invested in debt instruments such as bonds, fixed deposits, or cash equivalents.

For example, if an investor is 30 years old, the rule suggests keeping 70 percent of the portfolio in equities and 30 percent in debt. If the investor is 60 years old, then 40 percent should be in equities and 60 percent in debt.

This method links risk directly with age. As people grow older, their exposure to market volatility is reduced automatically. This makes the rule easy to follow and suitable for long term financial planning.

Also Read: The Rule of 114 for Tripling: How Fast Can Your Money 3x?

Why This Rule Was Created?

The logic behind this rule comes from the relationship between time and risk. Younger investors have many earning years ahead of them. They can recover from market losses and benefit from long term compounding. Older investors have less time to rebuild their savings if markets fall sharply.

The rule follows the lifecycle investing model. During early working years, the focus is on wealth creation. During later years, the focus shifts to capital protection and income stability.

This gradual shift helps avoid large financial shocks close to retirement. It also reduces emotional reactions during market ups and downs by providing a fixed structure.

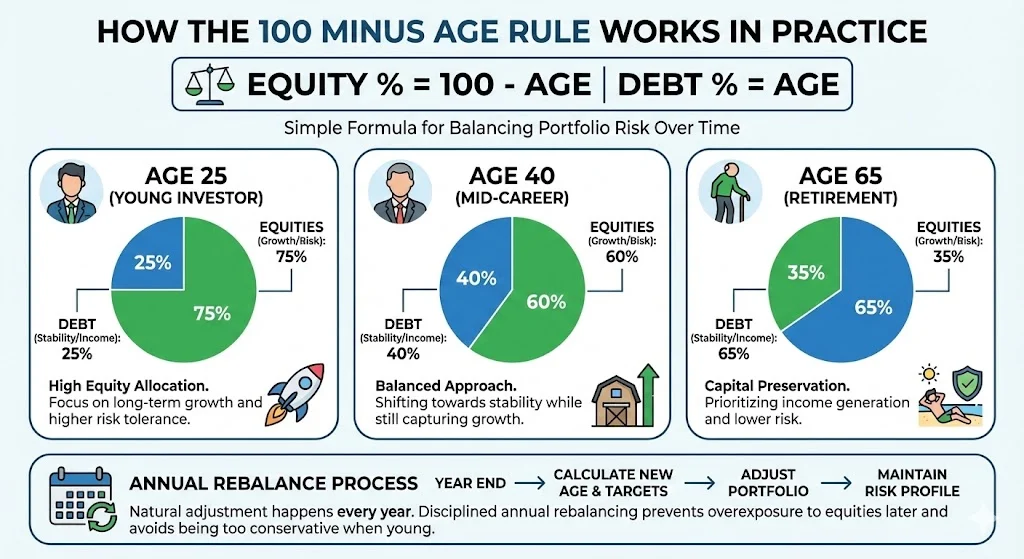

How The 100 Minus Age Rule Works in Practice?

The formula is straightforward.

Equity allocation percentage equals 100 minus your age.

Debt allocation percentage equals your age.

Examples:

- Age 25 means 75 percent in equities and 25 percent in debt.

- Age 40 means 60 percent in equities and 40 percent in debt.

- Age 65 means 35 percent in equities and 65 percent in debt.

This adjustment happens naturally every year. Investors who rebalance annually maintain the same risk profile relative to their age. This discipline prevents overexposure to equities during later years and avoids being too conservative when young.

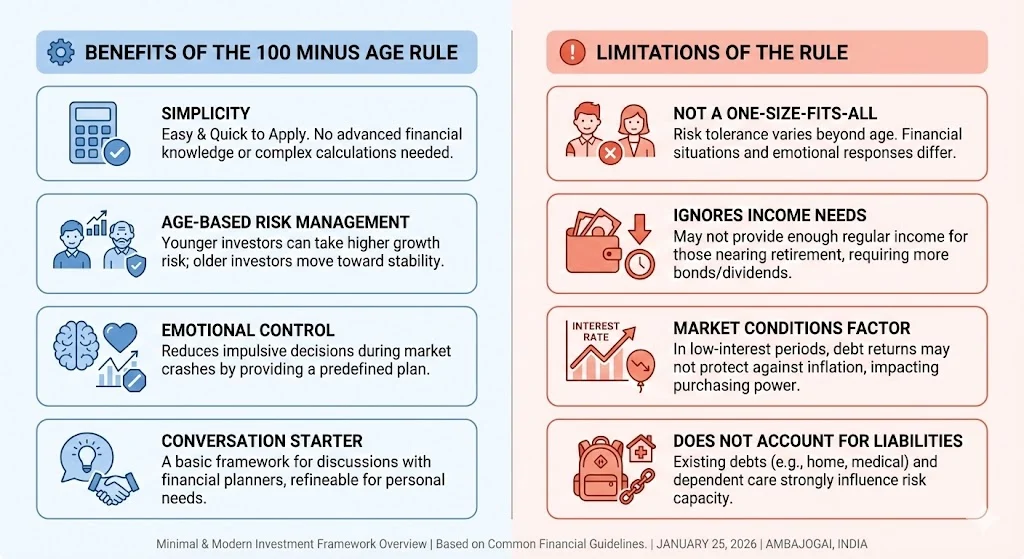

Benefits Of The 100 Minus Age Rule

The biggest strength of this rule is simplicity. It does not require advanced financial knowledge or complex calculations. Anyone can apply it in a few seconds.

It also supports age based risk management. Younger investors can take higher risk and aim for growth. Older investors move toward stability and income focused assets.

Another benefit is emotional control. During market crashes, many investors panic and sell. A predefined rule reduces impulsive decisions. Investors know exactly how much equity they should hold and are less likely to overreact.

The rule also works as a conversation starter with financial planners. It gives a basic framework that can be refined based on personal needs.

Limitations Of The 100 Minus Age Rule

Although useful, the rule does not fit every investor. Risk tolerance is not determined only by age. Two people of the same age can have very different financial situations and emotional responses to market volatility.

The rule also ignores income needs. Someone nearing retirement may require regular income from investments. This may require more bonds or dividend assets than the rule suggests.

Market conditions are another factor. During periods of low interest rates, debt returns may not protect against inflation. In such cases, very low equity exposure can hurt long term purchasing power.

The rule does not account for existing liabilities such as home loans, medical expenses, or dependent care. These factors strongly influence how much risk an investor can take.

Recent Trends and Evolving Views

In 2025 and 2026, financial discussions show that the rule is still widely referenced in education and mutual fund promotions. It is often taught as a basic asset allocation shortcut for beginners.

However, many experts now see it as overly conservative. With longer life expectancy and rising healthcare costs, retirees may need higher equity exposure to avoid running out of money.

This has led to modified versions such as:

- 110 minus age

- 120 minus age

These versions allow more equities at every age. For example, a 60 year old using the 120 rule would hold 60 percent in equities instead of 40 percent.

Public opinion from social media and forums shows that the rule is respected for its simplicity but rarely followed strictly. Most investors treat it as a reference point rather than a fixed command.

Public Opinion & Investor Sentiment ( Data From X )

Recent discussions show that most people view the rule as an educational tool. It is often shared along with other financial rules like budgeting formulas and withdrawal guidelines.

Some investors appreciate it as a safety net. It helps reduce risk near retirement and avoids heavy losses during market downturns.

Others criticize it for ignoring personal factors. A healthy 60 year old with stable income may safely hold more equities than the rule allows. A young person with heavy debt may need lower risk exposure despite age.

Overall sentiment suggests that the rule is useful for beginners but should evolve into a customized strategy over time.

Comparison With Modern Asset Allocation Approaches

Modern financial planning focuses on goal based and risk based allocation rather than age alone. Factors such as income stability, family responsibilities, health, and investment goals now play a larger role.

Instead of a simple equity and debt split, many portfolios include:

- Equities

- Debt

- Gold

- Real estate or REITs

- Cash reserves

This diversification improves stability and protects against inflation and economic cycles. The 100 Minus Age rule can still guide the equity portion while other assets add balance.

One Simple Allocation Example

Below is a basic illustration using the rule:

| Age | Equity Allocation | Debt Allocation |

|---|---|---|

| 30 | 70 percent | 30 percent |

| 45 | 55 percent | 45 percent |

| 60 | 40 percent | 60 percent |

This table shows how risk gradually reduces as age increases.

How to Use the Rule Wisely

The rule should be treated as a starting framework. Investors should adjust it based on personal comfort with risk and financial responsibilities.

Rebalancing once a year helps maintain discipline. It also prevents portfolios from becoming too aggressive or too conservative after market movements.

Combining this rule with goal planning improves outcomes. Short term goals may need more debt allocation while long term goals can use higher equity exposure.

Final Thoughts

The 100 Minus Age Asset Allocation rule remains one of the most practical tools for understanding risk and time in investing. It teaches the importance of shifting from growth to protection as life progresses.

In today’s environment, it should not be followed blindly. Longer lifespans, inflation, and changing markets require flexibility. Most experts agree that personalization is more important than rigid formulas.

Used correctly, the rule provides structure and emotional discipline. It helps investors stay invested during volatile periods and protect capital near retirement. As a foundation for financial planning, it still holds value when combined with individual goals and modern portfolio strategies.

Tags: asset allocation, personal finance, retirement planning, investment strategy, risk management, wealth building

Related Posts :

Share This Post