Tata Steel is one of the largest steel manufacturing companies in India and a important part of the Tata Group. The company was established in 1907 and is headquartered in Mumbai, India. It manages everything from iron ore mining to finished steel production.

The company manufactures hot rolled steel, cold rolled steel, galvanized steel, automotive grade steel, construction steel, and engineering products. Tata Steel plays an important role in India’s infrastructure growth. Its products are widely used in railways, automobiles, real estate, bridges, defense, and capital goods.

In this blog post we are going to see the share price target of tata steel for upcoming years from 2026-2030. And try to guess how much retuns can you expect from the tata steel. Also we are goin to look at numeric data like CAGR, EPS & ROE, Net profit from recent years to predict the future growth of tata steel.

Table of Contents

Tata Steel Share Price Target 2026

| Type | Target (₹) |

|---|---|

| Initial Target | 236.22 |

| Mid-Year Target | 273.87 |

| Year-End Target | 327.22 |

Tata Steel entered 2026 with strong momentum. In Q3 FY26, the company reported a sharp jump in consolidated net profit to around ₹2,700 crore. Revenue increased to nearly ₹57,000 crore for the quarter. EBITDA also improved significantly. This growth was mainly supported by strong domestic demand and better performance from its Netherlands operations.

The company is also expanding capacity. A new plant in Ludhiana worth ₹3,200 crore is expected to start operations in March 2026. This facility uses electric arc furnace technology and scrap steel, which supports sustainability goals. With better pricing guidance and volume growth, 2026 could be a recovery year for margins if steel prices remain stable.

Tata Steel Share Price Target 2027

| Type | Target (₹) |

|---|---|

| Initial Target | 336.84 |

| Mid-Year Target | 390.53 |

| Year-End Target | 466.61 |

By 2027, Tata Steel may benefit from continued infrastructure spending in India. Government focus on roads, railways, defense manufacturing, and housing can support steel demand. The company is also investing in green mobility initiatives like electric trucks in West Bokaro to reduce logistics cost and carbon footprint.

However, there are global challenges. The European Union’s Carbon Border Adjustment Mechanism has entered the financial phase from 2026. Since a large portion of Indian steel exports go to Europe, this can impact margins. Tata Steel may shift export focus to the Middle East and Asian markets to balance this risk. Overall, 2027 performance will depend on domestic growth and export strategy.

Tata Steel Share Price Target 2028

| Type | Target (₹) |

|---|---|

| Initial Target | 480.34 |

| Mid-Year Target | 556.90 |

| Year-End Target | 665.38 |

In 2028, Tata Steel’s long term sustainability projects may start showing stronger results. The company successfully completed a one year thermal energy storage pilot at its Jamshedpur plant in partnership with Kraftblock GmbH. This project reduces fuel usage and cuts around 22,000 tonnes of CO2 annually. Such initiatives can improve cost efficiency over time.

The company has also infused capital of around USD 264 million into its Singapore based subsidiary T Steel Holdings Pte Ltd. This shows management’s commitment to strengthening global operations. If European units turn consistently profitable and domestic volumes grow at 6 percent CAGR, earnings stability can improve in the medium term.

Tata Steel Share Price Target 2029

| Type | Target (₹) |

|---|---|

| Initial Target | 684.96 |

| Mid-Year Target | 794.14 |

| Year-End Target | 948.83 |

By 2029, Tata Steel’s performance will largely depend on steel cycle conditions. Historically, the company saw peak revenue in FY2022 at ₹2,43,959 crore. After that, revenue declined due to global price correction and volume pressure. FY2025 revenue stood at ₹2,18,543 crore.

If global steel prices recover and domestic safeguard duties continue to protect Indian producers from cheap imports, margins can improve. At the same time, investors must watch the ongoing antitrust probe by the Competition Commission of India related to past price collusion allegations. Any major penalty may create short term volatility. Still, strong brand value and integrated operations give Tata Steel a competitive advantage.

Tata Steel Share Price Target 2030

| Type | Target (₹) |

|---|---|

| Initial Target | 976.75 |

| Mid-Year Target | 1,132.44 |

| Year-End Target | 1,353.03 |

By 2030, Tata Steel aims to position itself as a leader in low carbon steel production. Global investors are focusing more on ESG compliance. Companies with cleaner production methods may get better valuation multiples. Tata Steel’s push toward electric arc furnaces and waste heat recovery systems supports this transition.

India is expected to remain one of the fastest growing steel consuming nations. Urbanization, manufacturing push, and Make in India initiatives can support long term demand. If capacity utilization remains high and debt is controlled, 2030 could reflect stable long term growth backed by domestic fundamentals.

Should I Buy Tata Steel Share?

Tata Steel is focusing on capacity expansion, sustainability, and operational efficiency. The recent profit recovery in FY26 shows early signs of turnaround. The company continues to invest in R&D and green technology.

However, steel is a cyclical business. Earnings depend heavily on global prices, demand cycles, and government policies. Investors should track debt levels, margins, and export exposure carefully.

Before investing, always do your own research. Understand your risk profile. The stock market carries risk and returns are not guaranteed.

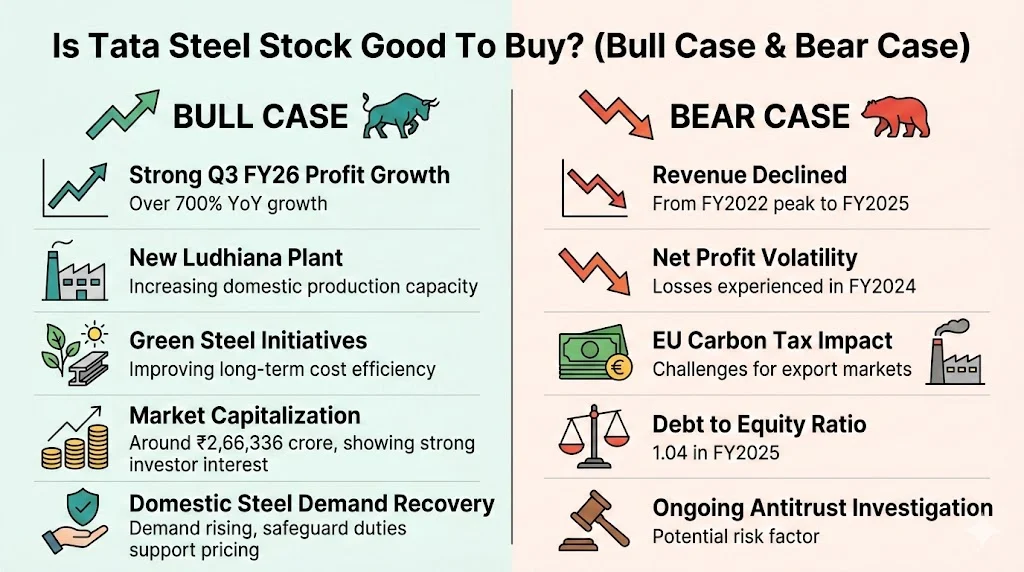

Is Tata Steel Stock Good To Buy? (Bull Case & Bear Case)

Bull Case

- Strong Q3 FY26 profit growth of over 700 percent YoY.

- New Ludhiana plant to increase domestic capacity.

- Green steel initiatives improving long term cost efficiency.

- Market cap around ₹2,66,336 crore showing strong investor interest.

- Recovery in domestic steel demand and safeguard duties support pricing.

Bear Case

- Revenue declined from FY2022 peak to FY2025.

- Net profit volatility with loss in FY2024.

- EU carbon tax impact on exports.

- Debt to equity at 1.04 in FY2025.

- Ongoing antitrust investigation risk.

Promoters Holding Of Tata Steel

| Category | Holding (%) |

|---|---|

| Promoters | ~33–34% |

| Public & Institutions | Remaining |

Promoter holding has remained stable over the last five years. Stable promoter stake reflects confidence of the Tata Group in long term business prospects.

Revenue Growth Of Tata Steel

| Year | Revenue (₹ Cr) | YoY Growth |

|---|---|---|

| FY2021 | 1,56,294 | 11.8% |

| FY2022 | 2,43,959 | 56.1% |

| FY2023 | 2,43,353 | -0.3% |

| FY2024 | 2,29,171 | -5.8% |

| FY2025 | 2,18,543 | -4.6% |

Revenue peaked in FY2022 due to high steel prices. After correction, revenue declined but remains strong compared to FY2021 levels.

Profit Growth (CAGR%) Of Tata Steel

| Year | Net Profit (₹ Cr) |

|---|---|

| FY2021 | 8,190 |

| FY2022 | 41,749 |

| FY2023 | 8,075 |

| FY2024 | -4,910 |

| FY2025 | 3,174 |

Profit has been highly volatile due to steel price cycles. FY2025 shows recovery after FY2024 loss.

EPS & ROE Trends Of Tata Steel

| Year | EPS (₹) | ROE (%) |

|---|---|---|

| FY2021 | 6.26 | 9.3 |

| FY2022 | 32.88 | 36.0 |

| FY2023 | 7.17 | 7.5 |

| FY2024 | -3.55 | -5.3 |

| FY2025 | 2.74 | 3.89 |

Return ratios declined after FY2022 peak. Improvement in future years will depend on stable margins.

Debt To Equity Ratio Of Tata Steel

| Year | Debt to Equity |

|---|---|

| FY2021 | 1.19 |

| FY2022 | 0.66 |

| FY2023 | 0.82 |

| FY2024 | 0.95 |

| FY2025 | 1.04 |

Debt increased slightly in FY2025. Managing leverage will be important for long term growth.

Net Profit Margins Of Tata Steel

| Year | Net Margin |

|---|---|

| FY2021 | 5.2% |

| FY2022 | 17.1% |

| FY2023 | 3.3% |

| FY2024 | -2.1% |

| FY2025 | 1.5% |

Margins are cyclical. FY2026 quarterly results show early signs of improvement.

Market Capitalization Of Tata Steel

| Year | Market Cap (₹ Cr) |

|---|---|

| Mar 2021 | ~1,50,000 |

| Mar 2022 | ~1,80,000 |

| Mar 2023 | ~1,70,000 |

| Mar 2024 | ~1,80,000 |

| Feb 2026 | 2,66,336 |

Rising market cap indicates renewed investor confidence after recent rally.

Dividend Yield Of Tata Steel

| Year | Dividend | Yield |

|---|---|---|

| FY2021 | 4.60 | 0.8% |

| FY2022 | 5.20 | 0.4% |

| FY2023 | 4.00 | 0.7% |

| FY2024 | 0 | 0% |

| FY2025 | ~3.50 | 1.68% |

Tata Steel is a consistent dividend payer, though payout depends on profitability.

Conclusion

Tata Steel is one of India’s leading steel producers with strong domestic presence and global operations. The company has faced revenue and profit volatility due to steel price cycles. However, FY26 results show strong recovery momentum. Capacity expansion, green steel initiatives, and domestic infrastructure growth are key positives.

Risks remain from global regulations, export pressure, and debt levels. Long term investors should monitor earnings stability and margin improvement.

Overall, Tata Steel remains a cyclical but fundamentally strong company. Investors should take decisions after proper research and risk assessment.