Suzlon Energy is one of India’s leading renewable energy companies with strong focus on wind turbine manufacturing and wind farm development. The company was founded in 1995 by Tulsi Tanti and is headquartered in Pune.

Suzlon provides end to end solutions which include design, manufacturing, installation, operation and maintenance of wind turbines. It has installed more than 18 GW capacity across 18 countries. In recent years Suzlon has gone through a major turnaround.

Revenue increased from about ₹3,346 Cr in FY21 to around ₹10,890 Cr in FY25. Profitability improved strongly after FY22 volatility. Net worth turned positive and the balance sheet became almost debt free. As of February 2026 the stock trades near ₹43 after correcting nearly 40 percent from its 2025 high of ₹74.

In this blog post we are going to see share price target of suzlon energy for year 2026-2040 by studying the quantitative data like cash flow, net revenue, dividend, EPS, debt to equity, etc

Table of Contents

Suzlon Energy Share Price Target 2026

| Month | Minimum Price (₹) | Maximum Price (₹) |

|---|---|---|

| January | 42 | 55 |

| December | 75 | 85 |

Suzlon entered FY26 with strong momentum. In Q3 FY26 the company reported revenue of around ₹4,236 Cr which was up about 42 percent YoY. It delivered 617 MW in the quarter and the order book stood at 6.4 GW. Recently Suzlon won a 248.85 MW wind order from ArcelorMittal in Gujarat. Gujarat remains a key state where Suzlon has installed base of around 4.5 GW.

However short term pressure is visible. The stock corrected due to mid cap weakness and analyst downgrades. Morgan Stanley downgraded the stock to equal weight with ₹52 target. Technical charts show support near ₹37 to ₹40 zone. Despite this the company remains operationally strong with focus on execution and margin improvement.

Suzlon Energy Share Price Target 2027

| Month | Minimum Price (₹) | Maximum Price (₹) |

|---|---|---|

| January | 95 | 120 |

| December | 160 | 170 |

By 2027 Suzlon aims to transform under its Suzlon 2.0 vision. In February 2026 Ajay Kapur was appointed as Group CEO. The company plans to evolve from pure wind player to full stack renewable company. It wants to expand into solar, battery energy storage systems and hybrid projects. This diversification can reduce cyclicality in wind business.

India’s renewable energy target of 500 GW non fossil capacity by 2030 creates large opportunity. Wind plus hybrid projects are gaining traction. If Suzlon maintains strong execution and wins large bids its revenue visibility will remain strong.

Suzlon Energy Share Price Target 2028

| Month | Minimum Price (₹) | Maximum Price (₹) |

|---|---|---|

| January | 140 | 170 |

| December | 200 | 210 |

By 2028 the impact of its new leadership and expansion strategy may become clearer. The company is focusing on larger capacity turbines like S144 series which improves efficiency. Higher capacity turbines help reduce levelized cost of power for clients.

Government policies also support wind sector. 100 percent FDI is allowed under automatic route. There is waiver of inter state transmission charges. National Repowering Policy 2023 supports replacement of old turbines with high capacity ones. These policies can create steady order inflow for Suzlon.

Suzlon Energy Share Price Target 2029

| Month | Minimum Price (₹) | Maximum Price (₹) |

|---|---|---|

| January | 180 | 205 |

| December | 235 | 240 |

By 2029 Suzlon’s hybrid and storage portfolio may contribute meaningfully. Battery storage integration is becoming important due to grid stability needs. If the company executes hybrid projects successfully it can improve margins and reduce earnings volatility.

Still investors must watch regulatory risks. Proposed stricter Deviation Settlement Mechanism rules can increase forecasting penalties for wind developers. Such rules can impact sector sentiment if implemented aggressively.

Suzlon Energy Share Price Target 2030

| Month | Minimum Price (₹) | Maximum Price (₹) |

|---|---|---|

| January | 210 | 235 |

| December | 270 | 275 |

By 2030 India’s renewable push will be at advanced stage. Suzlon with strong domestic presence can benefit from repowering and offshore wind opportunities. Budget 2026 increased allocation for renewable sector and MNRE initiatives. This creates long term demand visibility.

Execution remains key. Suzlon’s order book of 6.4 GW provides near term revenue visibility. If margins sustain in mid teens range then profitability can compound steadily.

Suzlon Energy Share Price Target 2040

| Month | Minimum Price (₹) | Maximum Price (₹) |

|---|---|---|

| January | 390 | 410 |

| December | 540 | 560 |

By 2040 renewable energy may dominate India’s power mix. Suzlon’s early mover advantage and installed base can give strong service revenue. Operation and maintenance contracts provide stable cash flow.

If the company successfully builds solar and storage verticals then it can become diversified renewable platform. Long term investors may benefit from structural clean energy shift.

Suzlon Energy Share Price Target 2050

| Month | Minimum Price (₹) | Maximum Price (₹) |

|---|---|---|

| January | 780 | 820 |

| December | 950 | 980 |

By 2050 global decarbonisation goals may increase demand for wind energy. Suzlon’s experience of more than five decades by then can position it as legacy renewable brand. Technology upgrades and offshore wind expansion can create additional revenue streams.

Long term outlook depends on innovation and capital discipline. Renewable energy is capital intensive sector so balance sheet strength will remain crucial.

Should I Buy Suzlon Energy Share?

Suzlon is focusing on diversification, margin improvement and strong execution. The company is investing in new turbine platforms and hybrid solutions. It has reduced debt and improved net worth.

However the stock is volatile. It corrected sharply in 2026 and sentiment is mixed. Investors should consider their risk profile. Always do your own research and understand risks before investing.

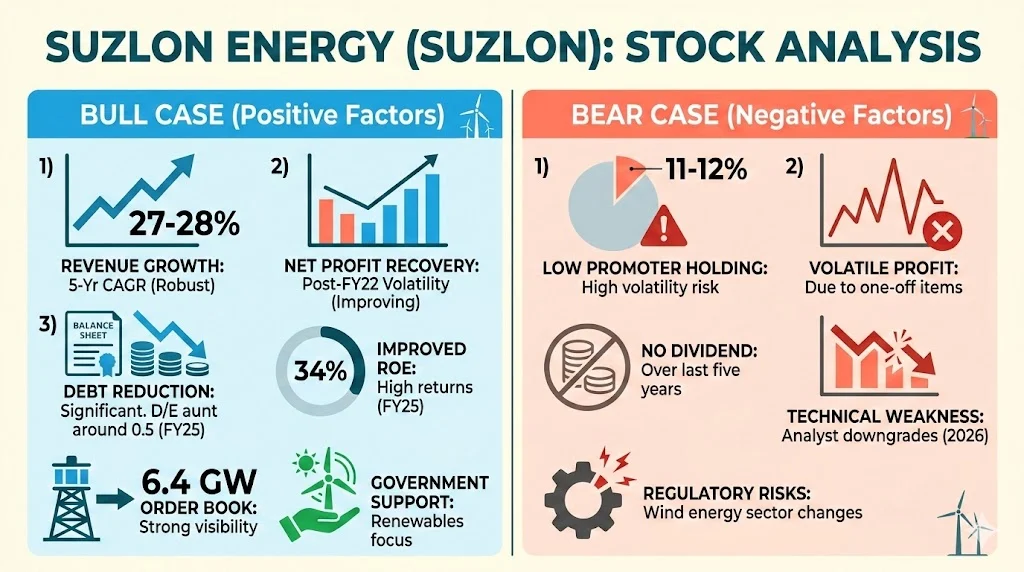

Is Suzlon Stock Good to Buy (Bull Case & Bear Case)

Bull Case

- Strong revenue CAGR of around 27 to 28 percent over last five years.

- Net profit recovery after FY22 volatility.

- Debt reduced significantly and D E around 0.5 in FY25.

- ROE improved to around 34 percent in FY25.

- Order book of 6.4 GW gives strong visibility.

- Government support for renewable sector.

Bear Case

- Promoter holding around 11 to 12 percent which is low.

- Profit highly volatile due to one off items.

- No dividend in last five years.

- Technical weakness and analyst downgrades in 2026.

- Regulatory risks in wind sector.

Revenue Growth

| Year | Revenue ₹ Cr | YoY % |

|---|---|---|

| FY21 | 3,346 | Base |

| FY22 | 6,582 | 97% |

| FY23 | 5,971 | -9% |

| FY24 | 6,529 | 9% |

| FY25 | 10,890 | 67% |

Revenue CAGR is around 27 to 28 percent. Growth in FY25 was very strong due to execution and large orders.

Profit Growth

| Year | Net Profit ₹ Cr |

|---|---|

| FY21 | 104 |

| FY22 | -177 |

| FY23 | 2,887 |

| FY24 | 660 |

| FY25 | 2,072 |

Profit is volatile. FY23 had one time gains. Sustainable margin appears in low to mid teen range.

EPS and ROE

| Year | EPS ₹ | ROE % |

|---|---|---|

| FY23 | 2.28 | High |

| FY24 | 0.49 | 16-17 |

| FY25 | 1.53 | 33-40 |

ROE improvement in FY25 shows better capital efficiency.

Debt to Equity Ratio of Suzlon Energy Ltd

| Financial Year | Total Debt (₹ Cr) | Equity (₹ Cr) | D/E Ratio |

|---|---|---|---|

| FY21 | ~1,166 | Negative Net Worth | NA |

| FY22 | ~1,059 | Negative Net Worth | NA |

| FY23 | ~866 | Negative / Low Equity | High |

| FY24 | ~886 | ~1,199 | ~0.74 |

| FY25 | ~1,780 | ~3,374 | ~0.53 |

Suzlon’s debt profile has improved significantly. Earlier the company had negative net worth due to accumulated losses. From FY24 onwards equity turned positive and strengthened further in FY25.

A D/E ratio of around 0.53 in FY25 indicates moderate leverage. It is not completely debt free but the balance sheet is much healthier than the past stress years. Lower debt reduces interest burden and improves profit stability.

Net Profit Margin of Suzlon Energy Ltd

| Financial Year | Revenue (₹ Cr) | Net Profit (₹ Cr) | Net Profit Margin (%) |

|---|---|---|---|

| FY21 | ~3,346 | ~104 | ~3% |

| FY22 | ~6,582 | ~-177 | ~-2.7% |

| FY23 | ~5,971 | ~2,887 | ~48%* |

| FY24 | ~6,529 | ~660 | ~10% |

| FY25 | ~10,890 | ~2,072 | ~19% |

*FY23 margin was abnormally high due to one time gains and write backs.

Net margin trend shows clear turnaround. FY22 was a loss year. FY24 and FY25 show more stable operating performance. A 19 percent margin in FY25 is strong for capital goods sector. Investors should focus on sustainable margins rather than one time spikes.

Market Capitalization of Suzlon Energy Ltd

| Financial Year | Approx. Market Cap (₹ Cr) |

|---|---|

| FY21 | ~10,000–15,000 |

| FY22 | ~15,000–20,000 |

| FY23 | ~25,000–30,000 |

| FY24 | ~35,000–40,000 |

| FY25 | ~58,000–60,000 |

Market capitalization has grown sharply over the last five years. This reflects improved profitability, debt reduction and strong investor interest in renewable theme.

However market cap expansion also means expectations are high. Future growth must justify current valuation levels.

Dividend Yield of Suzlon Energy Ltd

| Financial Year | Dividend Per Share (₹) | Dividend Yield (%) |

|---|---|---|

| FY21 | 0.00 | 0.00% |

| FY22 | 0.00 | 0.00% |

| FY23 | 0.00 | 0.00% |

| FY24 | 0.00 | 0.00% |

| FY25 | 0.00 | 0.00% |

Suzlon has not declared any dividend in the last five years. Dividend yield remains zero percent.

This shows the company is reinvesting profits into business expansion and balance sheet strengthening. Income focused investors may not find it attractive. Growth focused investors may still consider it.

Promoter Holding of Suzlon Energy Ltd

| Financial Year | Promoter Holding (%) |

|---|---|

| FY21 | ~15–18% |

| FY22 | ~14–16% |

| FY23 | ~13–15% |

| FY24 | ~12–13% |

| FY25 | ~11–12% |

Promoter holding has gradually reduced over the years. Current holding around 11 to 12 percent is relatively low compared to many Indian companies.

Low promoter stake means limited skin in the game. However high retail and institutional participation

Conclusion

Suzlon Energy Ltd has completed a major turnaround. Revenue crossed ₹10,000 Cr in FY25. Profitability improved and debt reduced. Order book is strong and government support for renewable sector remains intact.

Short term sentiment is weak due to correction and technical pressure. Long term story depends on execution, diversification into solar and storage, and stable margins.

Suzlon is a high risk high reward renewable stock. Investors with long term horizon and high risk appetite may consider tracking it closely. Always study financial statements and sector trends before making investment decision.