New RBI Credit Rules For Brokers: Big Shift In Leverage Game From April 2026

New RBI Credit Rules For Brokers Big Shift In Leverage Game From April 2026

The new RBI credit rules for brokers have suddenly become the hottest topic in Dalal Street circles. If you are tracking capital market stocks or active in F&O, you must have seen the sharp reaction after the announcement. Brokerage shares corrected heavily and traders started asking one simple question. Is this the end of easy leverage?

In mid February 2026, the Reserve Bank of India amended its Commercial Banks Credit Facilities Directions, 2026. These rules will be applicable from April 1, 2026. The focus is clear. Reduce systemic risk, control excessive leverage and stop indirect funding of speculative proprietary trading through banks. Let us break this down in simple language so you actually understand what is changing and why it matters.

Key Takeaways

- 100 percent collateral is now mandatory for bank loans to capital market intermediaries

- Banks cannot fund proprietary trading by brokers

- Bank guarantees require at least 50 percent collateral with minimum 25 percent cash

- Margin Trading Facility funding must be fully secured with high cash component

- Equity shares used as collateral will face minimum 40 percent haircut

- Brokerage and exchange stocks like BSE, Angel One and Groww reacted sharply

- Retail investors are not directly targeted but indirect impact is possible

- Public opinion is divided between stability supporters and active traders

What Exactly Has RBI Changed In 2026

Under the amended framework, all credit facilities extended by banks to Capital Market Intermediaries must be fully secured. This includes stock brokers, clearing members, custodians and market makers.

Earlier, there was some flexibility. Now there is no shortcut. After applying haircuts, exposure must be covered 100 percent with eligible collateral.

The rules come into force from April 1, 2026 and apply to fresh and renewed facilities.

Also Read: Kwality Wall’s Share: 26% Discount Debut Sparks Big Questions For Investors

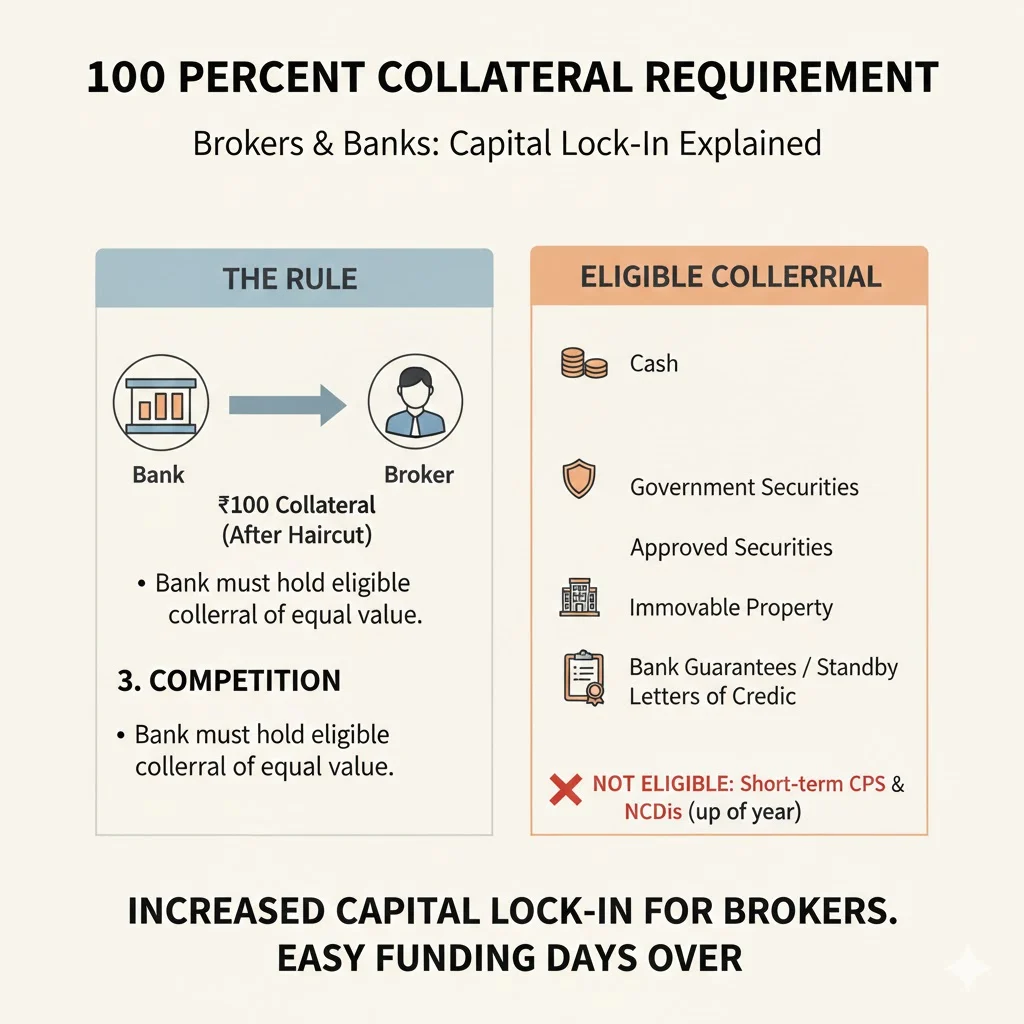

100 Percent Collateral Requirement Explained

This is the biggest shift. If a broker takes ₹100 exposure from a bank, the bank must hold eligible collateral of equal value after haircut.

Eligible collateral includes:

- Cash

- Government securities

- Approved securities

- Immovable property

- Receivables

- Bank guarantees

- Standby letters of credit

Short term commercial papers and short term NCDs up to one year cannot be used.

This directly increases capital lock-in for brokers. Easy funding days are clearly over.

Ban On Funding Proprietary Trading

The circular clearly states that banks shall not provide finance to a capital market intermediary for acquisition of securities on its own account.

In simple words, no bank money for proprietary trading.

There is a narrow exception for limited market making or genuine working capital mismatches. But even there, strict collateral rules apply.

Earlier, some brokers used structures like fixed deposits to indirectly obtain leveraged bank guarantees for prop desks. That route is now shut.

This is a structural change. Not just a temporary tightening.

Stricter Norms For Bank Guarantees

Bank guarantees issued to exchanges and clearing corporations now require:

- Minimum 50 percent collateral

- At least 25 percent in cash

If the guarantee relates to proprietary trading, it must be fully secured. Out of that, 50 percent must be cash.

This will increase operational cost. Cash is expensive. Blocking large cash margins impacts return on capital.

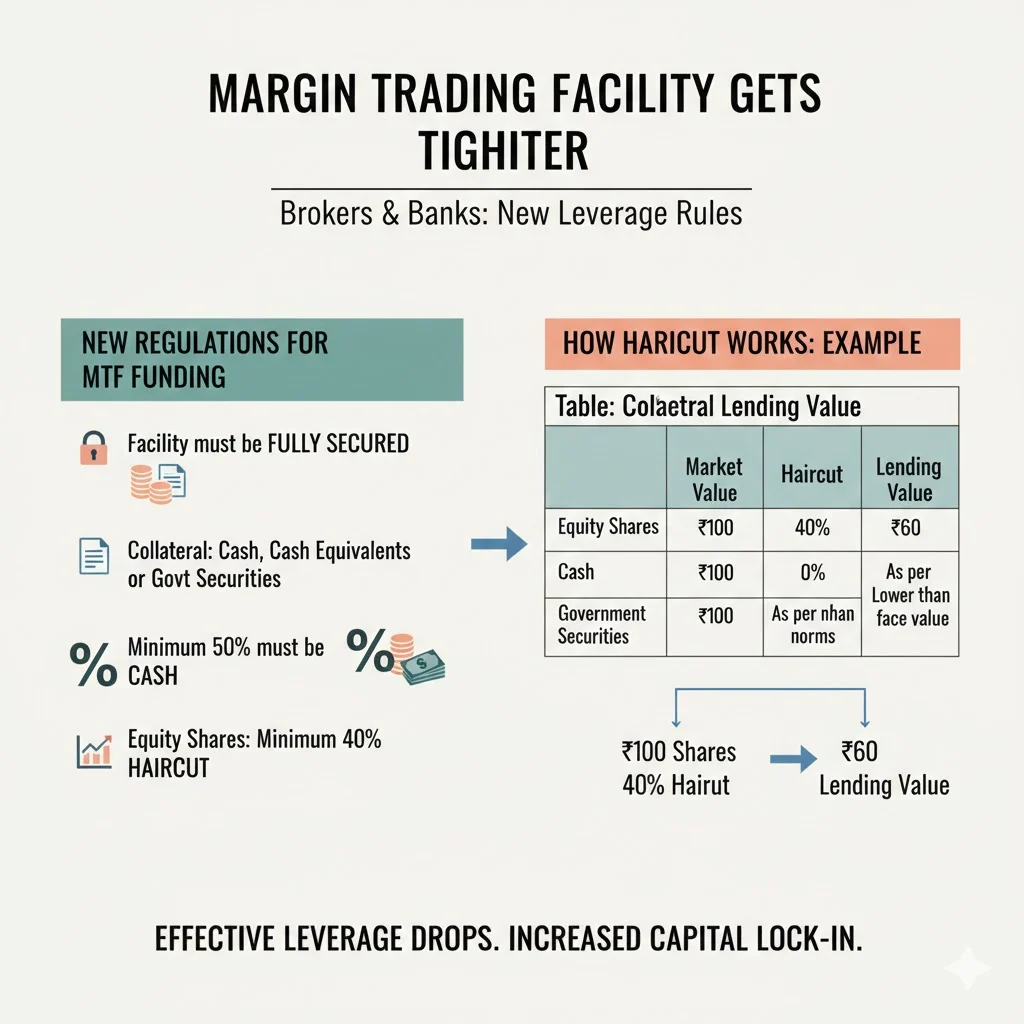

Margin Trading Facility Gets Tighter

Margin Trading Facility has grown into a more than ₹1 trillion market in India. Under this facility, brokers provide leverage to clients.

Now, if banks fund brokers for MTF:

- The facility must be fully secured

- Collateral must be cash, cash equivalents or government securities

- Minimum 50 percent must be cash

- Equity shares face minimum 40 percent haircut

Let us see how haircut works.

| Collateral Type | Market Value | Haircut | Lending Value |

|---|---|---|---|

| Equity Shares | ₹100 | 40 percent | ₹60 |

| Cash | ₹100 | 0 percent | ₹100 |

| Government Securities | ₹100 | As per norms | Lower than face value |

So if a broker pledges ₹100 worth shares, bank will consider only ₹60 for lending. Effective leverage drops automatically.

Exposure Limits Under Large Exposure Framework

All exposures to capital market intermediaries will be treated as capital market exposure.

Banks must set counterparty limits under the Large Exposure Framework.

This means a single broker cannot borrow unlimited funds from one bank. Concentration risk is being reduced.

Large brokerage firms that rely heavily on specific banking relationships may feel pressure.

Market Reaction After The Announcement

On February 16, 2026, capital market stocks corrected sharply.

- BSE fell up to around 9 to 10 percent intraday

- Angel One declined significantly

- Groww also saw selling pressure

Analysts estimated that proprietary trading accounts for nearly 40 to 50 percent of equity options turnover. With leverage drying up, F&O volumes could see 15 to 20 percent impact post April 2026.

This is serious for exchanges and brokers whose revenue depends on high volumes.

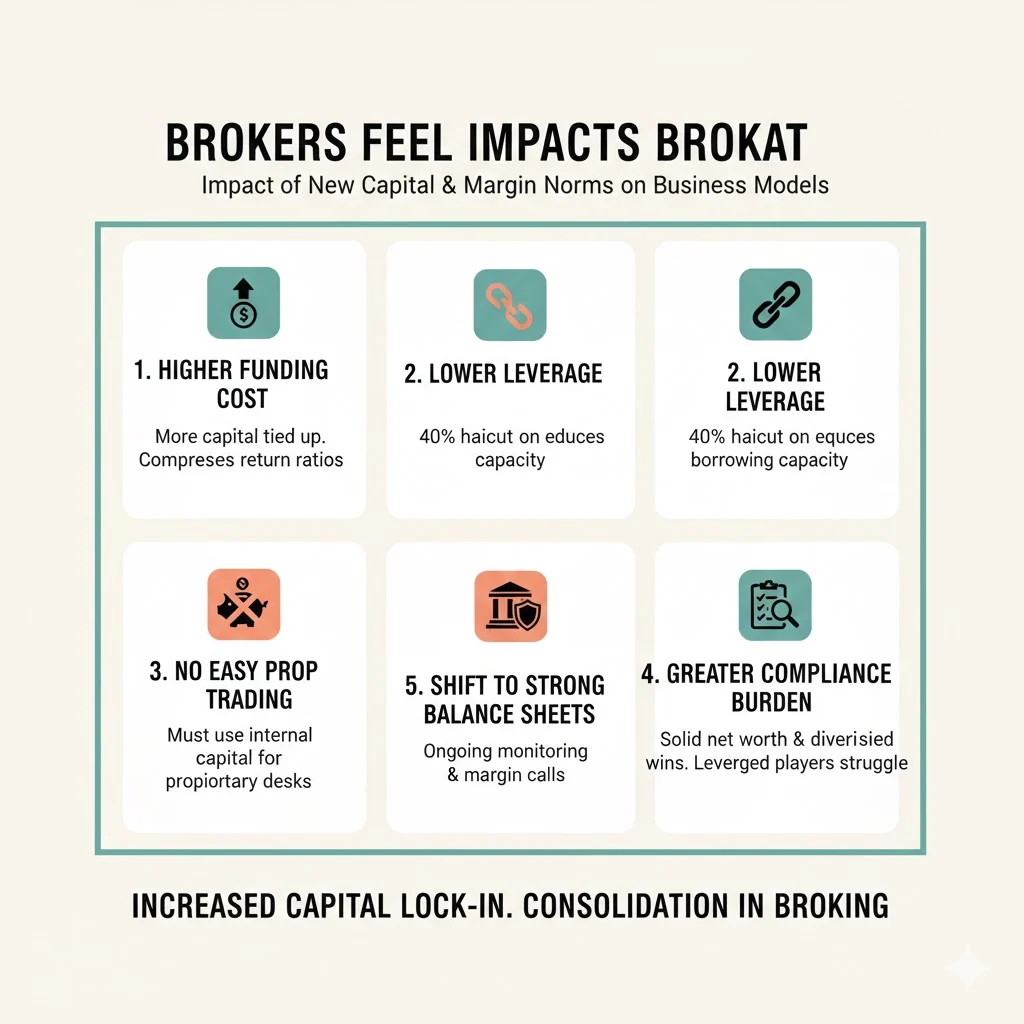

How New RBI Credit Rules Impacts Brokers?

Here is the real impact on brokerage business models.

- Higher Funding Cost: Full collateral means more capital tied up. Return ratios can compress.

- Lower Leverage: Minimum 40 percent haircut on equity reduces effective borrowing capacity.

- No Easy Prop Trading Funding: Brokers must use internal capital for proprietary desks.

- Greater Compliance Burden: Ongoing monitoring and margin calls for shortfall are mandatory.

- Shift Towards Strong Balance Sheets: Brokers with solid net worth and diversified funding will survive comfortably. Highly leveraged players may struggle.

Are Retail Investors Directly Affected

Directly, no.

The rules target bank to broker lending. Not retail trading accounts.

But indirectly:

- Brokers may reduce aggressive leverage offerings

- Intraday exposure limits may tighten

- Trading volumes in derivatives could moderate

- Cost structure might change over time

For long term investors, lower systemic leverage can actually be positive.

Public Opinion On X About New RBI Credit Rules

Public sentiment on X is mixed.

Many active traders feel this is a blow to high leverage prop trading. Comments suggest that easy leverage era is ending. Some users said intraday funding from banks may vanish.

Industry leaders also shared breakdowns explaining how previous workarounds are no longer possible. They called it a big structural change.

On the other side, long term investors welcomed the move. They believe this will reduce casino style F&O frenzy and protect the financial system.

Overall tone is cautious. Traders are worried about liquidity. Stability supporters are satisfied.

Bigger Picture Behind RBI Move

This step is not isolated.

Recently, transaction tax on derivatives was increased. Regulators have been signalling discomfort with excessive speculative activity.

The objective is clear:

- Protect banking system

- Prevent indirect funding of risky trading

- Reduce systemic shocks during market corrections

When leverage builds up too much, corrections become painful. RBI is trying to cool the system before it overheats.

Will This Reduce Market Liquidity

Short term, yes possibly.

Proprietary desks contribute heavily to cash futures arbitrage and options market making. If funding costs rise, spreads may widen slightly.

But over the long run, markets may become healthier. Volume may reduce but stability could improve.

It is basically a trade off between speed and safety.

Final Thoughts

The new RBI credit rules for brokers mark a serious shift in India’s capital market ecosystem. From April 1, 2026, leverage will be more expensive, proprietary trading will not get bank support and collateral discipline will be strict.

For traders who loved high leverage, this feels like a setback. For regulators focused on financial stability, this is a necessary correction.

Now the game will favour brokers with strong capital, disciplined risk management and clean balance sheets.

April 2026 will be interesting. Very interesting.

Related Posts :

Share This Post