Lloyds Engineering Share Price Target 2026, 2027, 2028, 2029, 2030

Lloyds Engineering Share Price Target 2026, 2027, 2028, 2029, 2030 | Image Via © lloydsengg.in

Lloyds Engineering also know as Lloyds Steels Industries, is an Indian engineering and heavy manufacturing company that is established in 1974 and its headwater is located in in Mumbai, Maharashtra.

The company operates a major manufacturing unit in Murbad, Thane district. It designs and manufactures critical equipment for hydrocarbons, oil and gas, steel plants, power plants, nuclear sector, marine, ports, and EPC projects.

Its product portfolio includes pressure vessels, reactors, heat exchangers, marine loading arms, structural equipment, and turnkey engineering solutions. The company supplies to major clients like IOCL, BPCL, HPCL, NPCIL, ISRO, Indian Navy, and other public and private sector companies.

In this blog post we are going to see the share price target of the Lloyds Engineering works from 2026 – 2050. Along with the share price target you will get the latest news, quotative data related to the Lloyds Engineering from which you can also able to predict the future growth of this company..

Lloyds Engineering Works Ltd Share Price Target 2026

| Month | Target Price (₹) |

|---|---|

| January 2026 | 98 |

| December 2026 | 120 |

After strong revenue recovery post FY23, the company has shown stable execution in hydrocarbons, steel, and power equipment segments. Revenue has grown significantly from ₹309 Cr in FY23 to ₹746 Cr in FY25. This reflects strong order inflow and better project execution.

The company is also focusing on margin improvement. Net profit increased to ₹99.73 Cr in FY25. Net profit margins improved to 13.3 percent. Debt levels are low with a debt to equity ratio of just 0.079 in FY25. This gives financial stability for future expansion. If order inflow continues from nuclear, marine, and refinery projects, FY26 can remain a strong growth year.

Lloyds Engineering Works Ltd Share Price Target 2027

| Month | Target Price (₹) |

|---|---|

| January 2027 | 123 |

| December 2027 | 145 |

By 2027, the company’s long term engineering contracts from oil and gas, marine loading systems, and power sector projects can reflect in stronger revenue visibility. Lloyds is one of the few Indian companies manufacturing fully hydraulic marine loading arms. This gives it a niche advantage.

Its collaboration history with global companies and approvals from agencies like Engineers India and MECON strengthen its credibility. Increasing government spending on infrastructure and refinery capacity expansion may support order book growth. With improving ROE which reached above 15 percent in FY25, capital efficiency is clearly improving.

Lloyds Engineering Works Ltd Share Price Target 2028

| Month | Target Price (₹) |

|---|---|

| January 2028 | 150 |

| December 2028 | 180 |

The company is registered with nuclear and atomic energy departments for specialized equipment supply. Nuclear and defense projects usually provide long term stable contracts. If India increases nuclear capacity and refinery expansion, Lloyds can benefit.

Revenue CAGR over the last five years stands around 61 percent. Profit CAGR is even higher due to operating leverage. If the company maintains execution discipline and cost control, operating margins may remain healthy. Expansion in heavy fabrication capacity can further strengthen growth visibility by 2028.

Lloyds Engineering Works Ltd Share Price Target 2029

| Month | Target Price (₹) |

|---|---|

| January 2029 | 81.23 |

| December 2029 | 86.25 |

By 2029, scale advantage can play a major role. Market capitalization has grown from around ₹50 Cr in FY21 to ₹5,717 Cr in FY25. This reflects strong investor confidence. Promoter holding currently stands near 49 percent, showing continued promoter interest though slightly reduced from earlier years.

The company’s presence in steel plant equipment and refinery process equipment places it in a strategic position as India focuses on manufacturing and energy security. If export orders increase, earnings diversification will improve further.

Lloyds Engineering Works Ltd Share Price Target 2030

| Month | Target Price (₹) |

|---|---|

| January 2030 | 300 |

| December 2030 | 350 |

Long term industrial growth in India supports companies like Lloyds Engineering. The government focus on Make in India, infrastructure expansion, and energy transition can generate sustained demand for heavy engineering products.

Return on Equity improved sharply after FY23. Efficient capital allocation and low debt levels provide flexibility for new capex or acquisitions. If management maintains project delivery timelines and margin discipline, 2030 can reflect the benefits of scale and diversified project portfolio.

Should I Buy Lloyds Engineering Works Ltd Share?

The company has shown strong revenue and profit growth since FY23. Revenue CAGR is around 61 percent over five years. Net profit CAGR is significantly higher due to operating leverage. Debt levels are very low. ROE improved sharply.

The company operates in sectors like hydrocarbons, nuclear, marine, and steel. These sectors benefit from government capital expenditure. However, engineering businesses are project based and earnings can fluctuate.

Investors should check order book visibility, margin sustainability, and promoter holding trends before investing. Always do your own research and understand the risks involved in cyclical industries before making any investment decision.

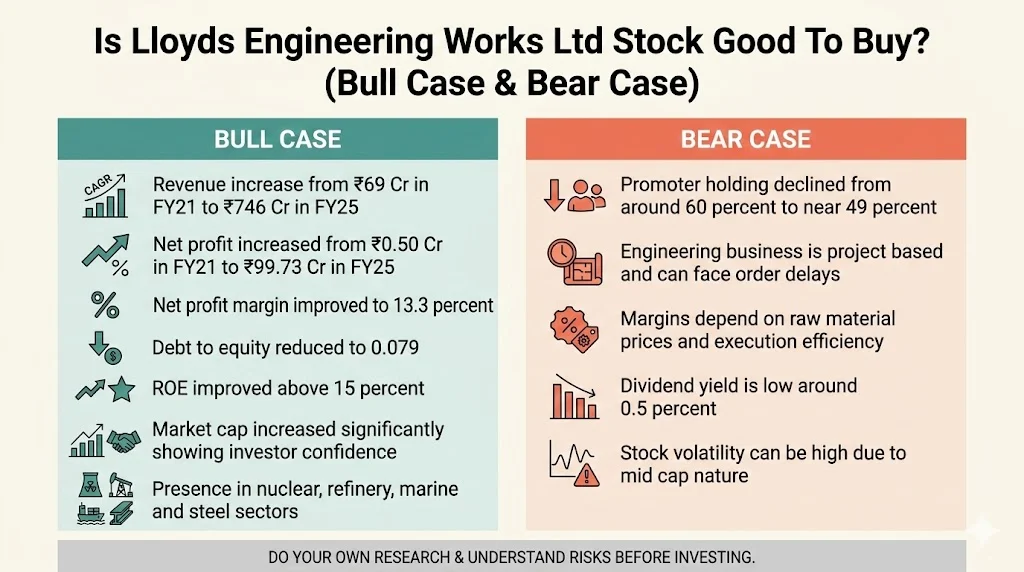

Is Lloyds Engineering Works Ltd Stock Good To Buy? (Bull Case & Bear Case

Bull Case

- Revenue increased from ₹69 Cr in FY21 to ₹746 Cr in FY25

- Net profit increased from ₹0.50 Cr in FY21 to ₹99.73 Cr in FY25

- Net profit margin improved to 13.3 percent

- Debt to equity reduced to 0.079

- ROE improved above 15 percent

- Market cap increased significantly showing investor confidence

- Presence in nuclear, refinery, marine and steel sectors

Bear Case

- Promoter holding declined from around 60 percent to near 49 percent

- Engineering business is project based and can face order delays

- Margins depend on raw material prices and execution efficiency

- Dividend yield is low around 0.5 percent

- Stock volatility can be high due to mid cap nature

Financial Snapshot of Lloyds Engineering Works Ltd

Promoters Holding Of Lloyds Engineering Works Ltd

| Year | Promoter Holding (%) |

|---|---|

| Mar-21 | 60 |

| Mar-22 | 56.2 |

| Mar-24 | 49.4 |

| Feb-26 | 49.26 |

Promoter holding has slightly declined but remains significant, indicating management involvement.

Revenue Growth Of Lloyds Engineering Works Ltd

| Year | Revenue (₹ Cr) |

|---|---|

| Mar-21 | 69.37 |

| Mar-23 | 309.72 |

| Mar-25 | 746.73 |

Strong revenue expansion shows successful order execution and scaling.

Profit Growth (CAGR%) Of Lloyds Engineering Works Ltd

| Year | Net Profit (₹ Cr) |

|---|---|

| Mar-21 | 0.50 |

| Mar-23 | 36.82 |

| Mar-25 | 99.73 |

Profit growth is strong post FY23 due to margin expansion.

EPS & ROE Trends Of Lloyds Engineering Works Ltd

| Year | EPS (₹) | ROE (%) |

|---|---|---|

| Mar-21 | 0.01 | 0.44 |

| Mar-24 | 0.74 | 19.42 |

| Mar-25 | 0.86 | 15.46 |

ROE improved significantly, reflecting better capital efficiency.

Debt To Equity Ratio Of Lloyds Engineering Works Ltd

| Year | D/E Ratio |

|---|---|

| Mar-23 | 0.242 |

| Mar-24 | 0.154 |

| Mar-25 | 0.079 |

Low and declining debt supports financial strength.

Net Profit Margins Of Lloyds Engineering Works Ltd

| Year | NPM (%) |

|---|---|

| Mar-23 | 11.9 |

| Mar-24 | 12.9 |

| Mar-25 | 13.3 |

Margins are stable and gradually improving.

Market Capitalization Of Lloyds Engineering Works Ltd

| Year | Market Cap (₹ Cr) |

|---|---|

| Mar-21 | 50 |

| Mar-24 | 3,000 |

| Mar-25 | 5,717 |

Massive increase in market cap reflects business turnaround.

Dividend Yield Of Lloyds Engineering Works Ltd

| Year | Dividend Yield (%) |

|---|---|

| Mar-24 | 0.49 |

| Mar-25 | 0.51 |

Dividend yield is modest. The company focuses more on growth and expansion.

Conclusion

Lloyds Engineering Works Ltd has shown a strong turnaround in the last few years. Revenue and profit growth are impressive. Debt levels are low and margins are improving. The company operates in strategic sectors like hydrocarbons, nuclear energy, marine systems, and steel plant equipment.

However, the engineering business is cyclical and project based. Order delays or margin pressure can affect earnings. Promoter holding has slightly reduced which investors should monitor.

Overall, from a financial research perspective, the company has demonstrated operational strength and improving fundamentals. Long term growth depends on sustained order inflow, margin control, and efficient capital allocation. Investors should evaluate risk appetite and conduct detailed research before investing.

Related Posts :

Share This Post