Cipla Share Price Falls 11% In 3 Months: Is This A Temporary Pharma Shock Or A Bigger Warning?

Cipla Share Price Falls 11% In 3 Months: Is This A Temporary Pharma Shock Or A Bigger Warning?

Cipla share price has corrected nearly 11% in the last three months. From around ₹1,530 levels in early January 2026, the stock is now trading in the ₹1,340 to ₹1,356 range. For many retail investors, this sudden drop feels confusing because Cipla is not a small company. It is one of India’s most respected pharma players with strong domestic presence and global operations.

So what exactly went wrong in Q3 FY26. Why are brokerages cutting targets. And more importantly, is this just short term pressure from the US market or something deeper. If you are tracking Cipla stock on NSE and thinking whether to buy, hold or wait, this detailed breakdown will help you understand the full picture.

Key Takeaways On Why Cipla Share Is Falling

- Cipla stock is down around 11% in the last 3 months

- Q3 FY26 PAT fell 57% YoY to ₹676 crore

- EBITDA dropped 37% and margins shrank to 17.7%

- US business revenue declined 22% YoY

- Lanreotide supply disruption and gRevlimid decline hit earnings

- FY26 EBITDA margin guidance cut to around 21%

- India business grew 10% YoY with strong chronic portfolio

- Net cash position remains strong at ₹10,229 crore

- Public sentiment on X is cautious but not panic driven

What Triggered The 11% Fall In Cipla Stock?

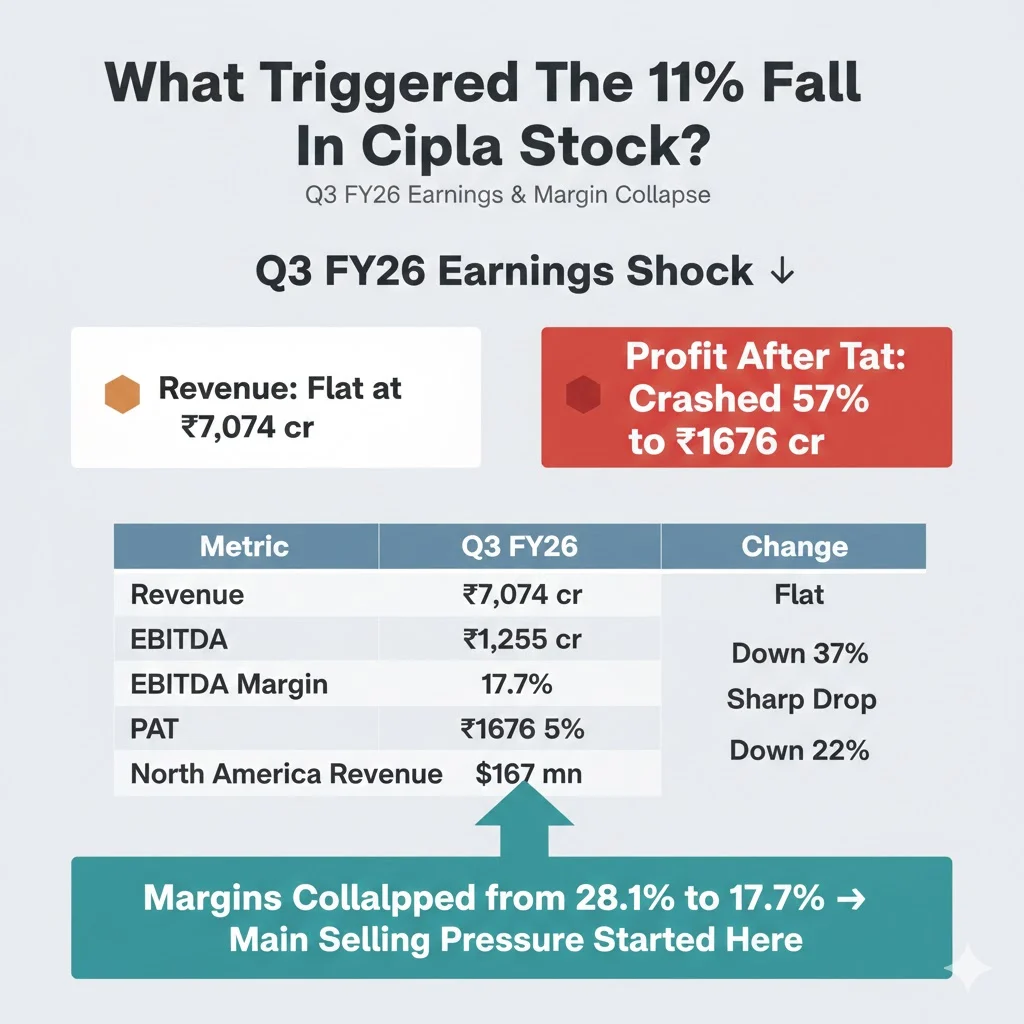

The biggest trigger was Q3 FY26 earnings. Revenue was flat at ₹7,074 crore. But profit after tax crashed 57% year on year to ₹676 crore. That shocked the Street.

Here is a quick snapshot of key numbers:

| Metric | Q3 FY25 | Q3 FY26 | Change |

|---|---|---|---|

| Revenue | ₹7,073 crore | ₹7,074 crore | Flat |

| EBITDA | Higher Base | ₹1,255 crore | Down 37% |

| EBITDA Margin | 28.1% | 17.7% | Sharp Drop |

| PAT | ₹1,570 crore approx | ₹676 crore | Down 57% |

| North America Revenue | Higher Base | $167 million | Down 22% |

Margins collapsing from 28% to 17.7% is not a small thing. That is where most of the selling pressure started.

Also Read: Jio Financial Services Share Falling: Why The Stock Slipped 16% In 3 Months Despite Big Hype

US Business Weakness Is The Core Problem

The main issue is in the North America segment. Cipla’s US revenue dropped 22% year on year. Two major products caused the pain.

First is generic Revlimid. This oncology drug was a high margin product. After exclusivity ended, competition increased. Volumes dropped. Realisations also came down.

Second is Lanreotide. Production was paused due to USFDA observations at a partner facility in Greece. This created supply disruption. Lanreotide contributes roughly $150 million annually for Cipla in the US. So even temporary disruption impacts earnings.

Brokerages flagged this as near term risk because supply is expected to normalise only in H1 FY27.

Margin Guidance Cut Added More Pressure

Management reduced FY26 EBITDA margin guidance to around 21%. Earlier guidance range was higher. This cut of 175 to 300 basis points made analysts cautious.

R&D spending also increased 37% year on year. It now stands at around 7% of sales. There was also a one time impact of ₹276 crore due to labour code changes.

So you have weaker US sales, higher R&D costs and one time expenses. All combined. That is why profitability took a big hit.

What Brokerages Are Saying Now?

Different brokerages have different views.

Some global firms downgraded the stock to Underperform or Hold. Target prices were cut to the ₹1,170 to ₹1,360 range. EPS estimates for FY27 were also reduced.

However, not everyone is bearish. Some maintained Buy or Outperform ratings with targets around ₹1,490 to ₹1,510. The argument is simple. Most bad news is already priced in after the recent correction.

This split view shows that the market is not writing off Cipla. It is just uncertain about near term recovery.

India Business Is Still Solid

Now here is the part that many headlines ignore.

Cipla’s India business grew around 10% year on year. Chronic therapies form nearly 62% of the domestic portfolio. Respiratory segment is outperforming the market.

Africa performance remains strong. Emerging markets and Europe have delivered over $100 million revenue for four consecutive quarters.

So while the US business is under stress, the core India franchise is stable. That matters in the long term story.

Balance Sheet Strength Gives Cushion

One more important point. Cipla has net cash of around ₹10,229 crore. Debt levels are low.

This strong balance sheet gives flexibility. The company can invest in R&D, manage supply disruptions and still stay financially stable.

In pharma sector, balance sheet strength is underrated. But during tough quarters, it makes a big difference.

Public Opinion On X Is Surprisingly Calm

When a stock falls 10% plus, usually social media becomes hyper negative. But that is not the case here.

On X, most discussions are:

- Traders sharing short term technical levels around ₹1,350

- Some calling it a bounce opportunity

- CSR related posts about Cipla Foundation activities

- Awards and recognition posts

There is no viral backlash. No panic selling narrative. Retail sentiment feels more wait and watch.

A few isolated complaints about specific inhaler products were seen. But nothing that created large scale negativity.

Overall mood is cautious, not fearful.

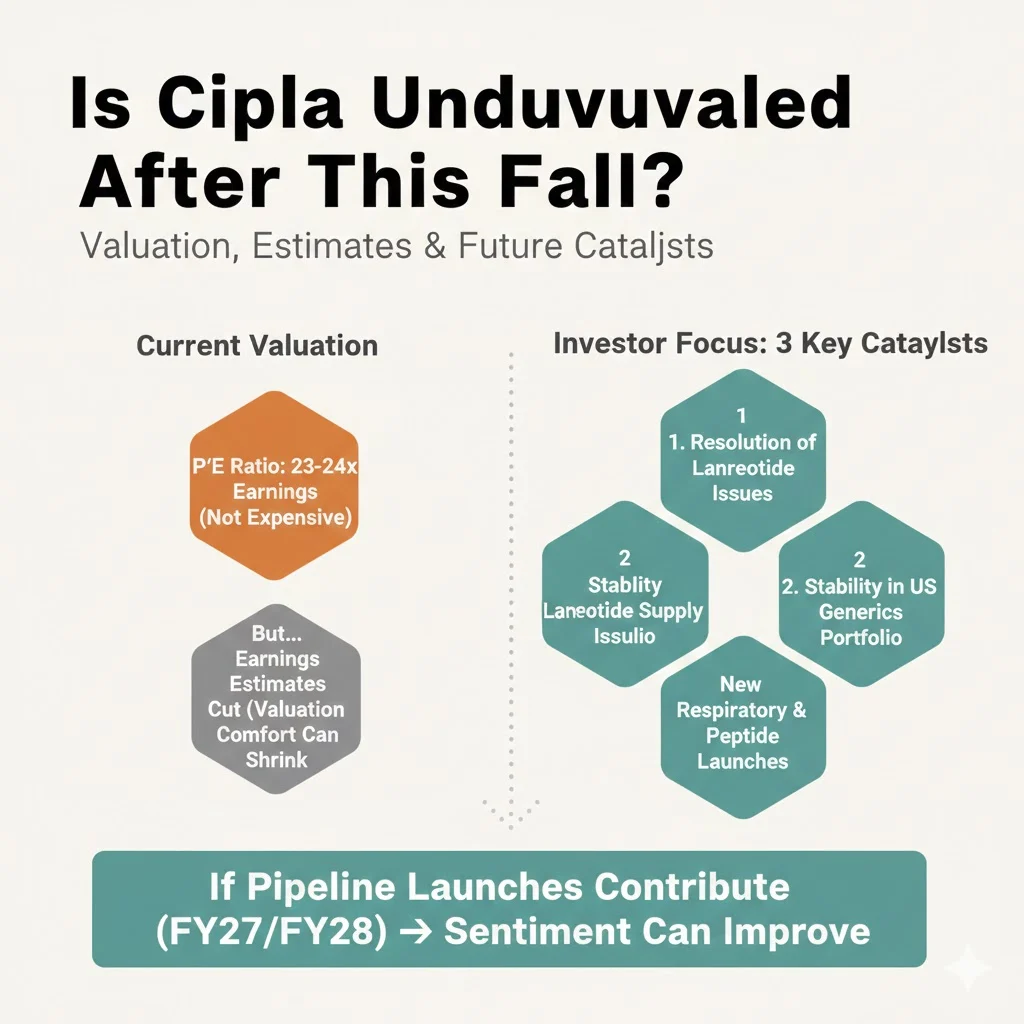

Is Cipla Undervalued After This Fall?

Valuation wise, Cipla is trading at around 23 to 24 times earnings. Compared to some pharma peers, that is not expensive.

But here is the catch. Earnings estimates have been cut. So if FY27 US revenues remain weak, the valuation comfort can shrink.

Investors are waiting for clarity on three key things:

- Resolution of Lanreotide supply issues

- Stability in US generic portfolio

- New respiratory and peptide launches

If pipeline launches start contributing meaningfully in FY27 and FY28, sentiment can improve.

Key Risks To Watch Going Ahead

Let us summarise the main risk factors clearly:

- Continued USFDA scrutiny

- Delayed restart of Lanreotide production

- Further price erosion in US generics

- Competition in gAdvair and other respiratory products

- Margin recovery slower than expected

If these risks ease, stock can stabilise. If they worsen, downside may continue in short term.

Long Term View Versus Short Term Volatility

Right now Cipla is facing short term headwinds. Most of them are US specific. India business remains steady. Africa and emerging markets are supporting growth.

The stock has already corrected around 11% in three months and nearly 12% year to date in some phases. That means a portion of bad news is priced in.

But pharma stocks usually move based on earnings visibility. Until clarity comes on US recovery and margin stabilisation, volatility can remain.

So this is not a story of structural collapse. It is a story of near term pressure versus long term fundamentals.

For investors, the decision depends on risk appetite. Traders are looking at technical bounce levels. Long term investors are watching execution and pipeline.

One thing is clear. Cipla is not in panic mode. It is in transition mode.

Conclusion

Cipla share price fall of 11% in three months is mainly due to weak Q3 FY26 results, US sales decline, Lanreotide disruption and margin guidance cut. The Street reacted strongly because profit dropped 57%.

However, India business growth, strong cash position and future product launches provide some support.

The next two quarters will be crucial. If US supply normalises and margins improve, confidence can return. Until then, the stock may remain range bound with cautious sentiment.

In markets, sometimes noise looks bigger than reality. For Cipla, the real test is execution in FY27.

Related Posts :

Share This Post