Adani Wilmar Share Price Target 2026, 2027, 2030, 2050

Adani Wilmar Share Price Target 2026, 2027, 2030, 2050 | Image Via © awl.in

Adani Wilmar that is now renamed as AWL Agri Business Ltd is India’s one of the leading FMCG and edible oil companies. Company is known for its Flagship brand “Fortune” that is very popular in Indian household.

AWL operates in a volume driven and competitive market where margins are directly proportional to the global commodity prices and import duties. After the complete exit of Adani Group, Wilmar International is now the sole promoter. Now company is focusing on increasing its food segment contribution and reducing dependence on edible oils to build a more stable and profitable business model.

In this blog post we are going to discuss about share price target of Adani Wilmar from 2026 – 2050. And try to find out how much returns can you expect from Adani Wilmar in upcoming years. I will give you all the latest news, numeric data bear & bull case conditions so that you will get overview of share price in upcoming years.

Table of Contents

Adani Wilmar Share Price Target 2026

| Month | Target Price |

|---|---|

| January 2026 | ₹385 |

| December 2026 | ₹540 |

In the year 2026 AWL is going through a transition phase. In Q3 FY26, revenue touched a record level of around ₹18,603 crore, which shows strong demand and distribution strength. However, profit after tax declined by around 35 percent to ₹269 crore due to margin pressure in edible oils. This shows that while volumes are strong, profitability depends heavily on raw material prices and import duties.

The acquisition of GD Foods, owner of the Tops brand, will strengthen its packaged food portfolio. The management has clearly stated that it wants the food segment to reach ₹10,000 crore by FY27. If this strategy works, 2026 can be a base building year for future growth.

Adani Wilmar Share Price Target 2027

| Month | Target Price |

|---|---|

| January 2027 | ₹550 |

| December 2027 | ₹770 |

By 2027, the impact of food segment expansion may become more visible. Currently, the food business has turned profitable and is growing fast through modern trade and quick commerce channels. The company is trying to reduce edible oil dependence and improve overall margins.

If revenue continues to grow at around 14 to 15 percent CAGR as seen in the last five years and margins stabilize above 2 percent, profitability can improve sharply. Institutional participation has also increased recently. If investor confidence returns after promoter restructuring, 2027 can show stronger earnings recovery compared to previous volatile years.

Adani Wilmar Share Price Target 2028

| Month | Target Price |

|---|---|

| January 2028 | ₹800 |

| December 2028 | ₹1,110 |

In 2028, AWL Agri Business may benefit from scale advantages. The company has steadily reduced its debt to equity ratio from 0.92 in FY21 to 0.21 in FY25. This strong balance sheet gives flexibility for expansion and acquisitions.

If food segment contribution rises to 30 to 35 percent of total revenue, earnings quality can improve. Edible oil margins are usually thin, but packaged foods offer better margin stability. With Wilmar International’s global sourcing expertise, the company can improve cost efficiency and exports. This can support long term earnings growth.

Adani Wilmar Share Price Target 2029

| Month | Target Price |

|---|---|

| January 2029 | ₹1,150 |

| December 2029 | ₹1,600 |

By 2029, the company’s strategy of becoming a complete food FMCG player may reflect in financial numbers. Revenue peaked at ₹61,573 crore in FY25 after a dip in FY24. Net profit also recovered strongly to ₹1,216 crore in FY25 after falling to ₹278 crore in FY24.

If the company maintains revenue growth above industry average and keeps debt under control, valuation re rating is possible. However, the sector remains competitive. Companies like ITC, Tata Consumer and other regional brands compete aggressively. Execution will be the key factor for 2029 growth.

Adani Wilmar Share Price Target 2030

| Month | Target Price |

|---|---|

| January 2030 | ₹1,650 |

| December 2030 | ₹2,300 |

By 2030 AWL Agri Business can position itself as a diversified FMCG company rather than just an edible oil player. India imports a large portion of edible oils, so any change in import duty directly affects margins. The government reduced customs duty in 2025 to control inflation. Such policy changes can create short term volatility.

If the company successfully balances edible oils, staples and packaged foods, it can build a more stable earnings model. Long term growth in Indian consumption, urbanization and rising middle class can support volume growth till 2030.

Adani Wilmar Share Price Target 2040

| Month | Target Price |

|---|---|

| January 2040 | ₹4,500 |

| December 2040 | ₹6,000 |

Looking at 2040, the company’s long term story depends on brand strength and distribution expansion. Fortune is already one of the most trusted edible oil brands in India. If AWL builds similar trust in packaged foods, ready to cook and value added products, margins can structurally improve.

The company’s ability to innovate, manage commodity cycles and maintain low debt will decide its 2040 growth potential. Strong global backing from Wilmar International can also help in technology, sourcing and export expansion.

Adani Wilmar Share Price Target 2050

| Month | Target Price |

|---|---|

| January 2050 | ₹9,000 |

| December 2050 | ₹12,000 |

By 2050, India’s population, income level and consumption pattern will be much higher than today. If AWL Agri Business continues expanding its portfolio and adapts to health trends such as premium oils, organic foods and value added staples, it can remain relevant.

However, long term investors must remember that commodity linked businesses always face cycles. Sustainable profitability and brand building will be more important than just revenue growth.

Should I Buy Adani Wilmar Share?

The company is focusing strongly on expanding its food segment. It has reduced debt significantly. Revenue CAGR from FY21 to FY25 is around 14.5 percent. Net profit CAGR is around 13.7 percent. FY25 showed strong recovery in profit and margins after a weak FY24.

On the negative side, net profit margins are still low at around 2 percent. The company does not pay dividend. The stock is trading near multi year lows around ₹190 to ₹191 as of February 2026. This shows weak market sentiment.

If you believe in long term consumption growth and management execution under Wilmar, it can be considered after proper research. Always do your own analysis and understand the risks before investing.

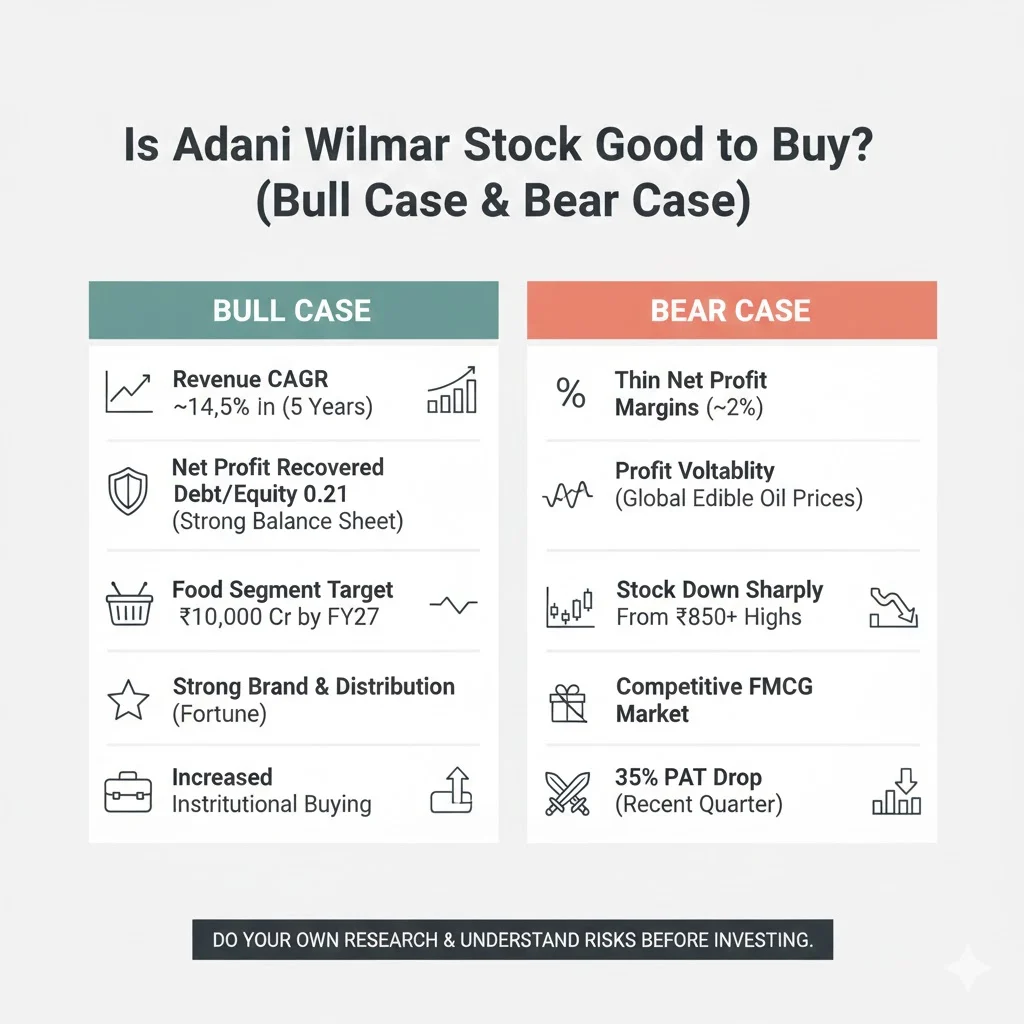

Is Adani Wilmar Stock Good to Buy? (Bull Case & Bear Case)

Bull Case

- Revenue CAGR of around 14.5 percent in last five years.

- Net profit recovered strongly in FY25 to ₹1,216 crore.

- Debt to equity reduced to 0.21 which shows strong balance sheet.

- Food segment target of ₹10,000 crore by FY27.

- Strong brand Fortune and wide distribution network.

- Institutional buying increased in recent quarters.

Bear Case

- Net profit margins remain very thin at around 2 percent.

- Profit volatility due to global edible oil prices.

- Stock has fallen sharply from historical highs above ₹850.

- No dividend payout despite profits.

- Competitive FMCG market with strong players.

- Recent quarter showed 35 percent drop in PAT due to margin pressure.

Promoters Holding of Adani Wilmar

| Year | Promoter Holding |

|---|---|

| FY22 | ~86.8% |

| FY23 | ~75%+ |

| FY24 | ~44% |

| FY25 | ~57% |

| Feb 2026 | ~57% |

Adani Group has fully exited. Wilmar International is now the sole promoter with majority control.

Revenue Growth of Adani Wilmar

| Year | Revenue (₹ Cr) |

|---|---|

| FY21 | 35,765 |

| FY22 | 52,254 |

| FY23 | 55,179 |

| FY24 | 49,136 |

| FY25 | 61,573 |

Revenue CAGR is around 14.5 percent despite volatility.

Profit Growth (CAGR%) of Adani Wilmar

| Year | Net Profit (₹ Cr) |

|---|---|

| FY21 | 729 |

| FY22 | 808 |

| FY23 | 607 |

| FY24 | 278 |

| FY25 | 1,216 |

Profit CAGR is around 13.7 percent. Profitability is volatile due to margin pressure.

EPS and ROE Trends of Adani Wilmar

| Year | EPS (₹) | ROE (%) |

|---|---|---|

| FY21 | 63.74 | ~20% |

| FY22 | 6.92 | ~11% |

| FY23 | 4.67 | 7.6% |

| FY24 | 2.14 | ~3.4% |

| FY25 | 9.36 | 13.9% |

ROE improved in FY25 after weak FY24.

Debt to Equity Ratio of Adani Wilmar

| Year | D/E Ratio |

|---|---|

| FY21 | 0.92 |

| FY22 | 0.36 |

| FY23 | 0.29 |

| FY24 | 0.32 |

| FY25 | 0.21 |

Debt has reduced significantly which is positive for long term stability.

Net Profit Margins of Adani Wilmar

| Year | Net Profit Margin |

|---|---|

| FY21 | 2.0% |

| FY22 | 1.5% |

| FY23 | 1.1% |

| FY24 | 0.6% |

| FY25 | 2.0% |

Margins are thin but recovered in FY25.

Market Capitalization of Adani Wilmar

| Year | Market Cap (₹ Cr) |

|---|---|

| FY22 | 1,31,600 |

| FY23 | 73,500 |

| FY24 | 71,800 |

| FY25 | 52,700 |

| Feb 2026 | 24,900 |

Market cap declined sharply from IPO peak due to stock correction.

Dividend Yield of Adani Wilmar

| Year | Dividend Yield |

|---|---|

| FY21 | 0.0% |

| FY22 | 0.0% |

| FY23 | 0.0% |

| FY24 | 0.0% |

| FY25 | 0.0% |

The company has not paid dividends so far and focuses on reinvestment.

Conclusion

Adani Wilmar, now AWL Agri Business Ltd, is transforming from an edible oil dominant company to a diversified food FMCG player. Revenue growth has been strong over five years, but profit margins remain thin and volatile. FY25 showed strong recovery in profit, reduced debt and improving ROE.

The stock is currently trading near multi year lows, which reflects weak sentiment and past volatility. Long term growth depends on successful food segment expansion, margin stability and execution under Wilmar International leadership.

For long term investors who understand commodity cycles and FMCG competition, this company can offer recovery potential. However, always study financials carefully and consider risk factors before making any investment decision.

Related Posts :

Share This Post