Kwality Wall’s Share: 26% Discount Debut Sparks Big Questions For Investors

Kwality Wall's Share: 26% Discount Debut Sparks Big Questions For Investors

Kwality Wall’s share has finally hit the stock market, and honestly, the debut was not what many investors expected. After the much-talked-about demerger from Hindustan Unilever, the stock listed at ₹29.80 on NSE, nearly 26 percent lower than the indicative price of around ₹40.20. That kind of discount immediately grabbed attention across Dalal Street.

But here is the real question. Is this weak listing a red flag or a long-term opportunity in India’s fast-growing ice cream market? With Kwality Wall’s now operating as an independent company under the name Kwality Wall’s India Ltd and trading under ticker KWIL, the game has changed. Let us break it down properly so you know what is actually happening behind the scenes.

Key Takeaways

- Kwality Wall’s listed at ₹29.80, nearly 26 percent below the indicative price.

- Market capitalisation debuted around ₹7,000 crore.

- The ice cream business contributes around ₹1,800 crore revenue, nearly 3 percent of HUL turnover earlier.

- Share entitlement ratio was 1:1 for HUL shareholders.

- Open offer announced to acquire up to 26 percent stake.

- Company holds around 10 percent market share in India’s ice cream segment.

- Investor sentiment is cautious but long-term growth story remains intact.

Also Read: New RBI Credit Rules For Brokers: Big Shift In Leverage Game From April 2026

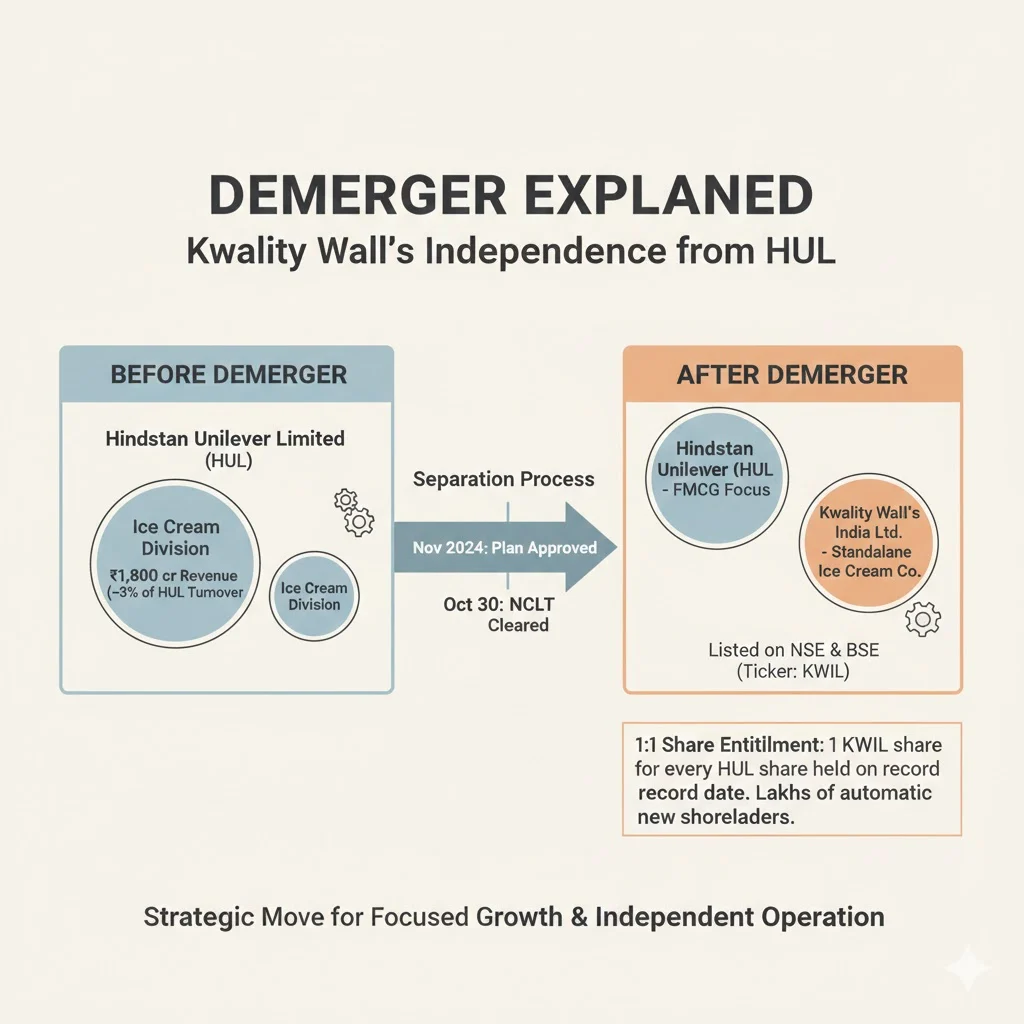

Demerger From Hindustan Unilever Explained

Kwality Wall’s was earlier part of Hindustan Unilever Limited. The demerger plan was approved in November 2024 and later cleared by the National Company Law Tribunal on October 30. The idea was simple. Separate the ice cream business and allow it to operate independently.

The ice cream division contributed about ₹1,800 crore revenue, which was roughly 3 percent of HUL’s annual turnover. Compared to HUL’s overall size, this segment was small but still significant in the frozen dessert category.

Under the 1:1 share entitlement ratio, every HUL shareholder received one share of Kwality Wall’s for each HUL share held on the record date. That made the listing highly anticipated because lakhs of investors automatically became shareholders of the new entity.

Now as a standalone company, Kwality Wall’s India Ltd is listed on both NSE and BSE under the ticker KWIL.

Also Read: Income Tax Exemption On Meal Cards: ₹1.05 Lakh Tax Free Benefit Under Draft Rules 2026 Explained

Listing Day Performance And Market Reaction

Here is what actually happened on debut day.

| Particulars | Details |

|---|---|

| NSE Listing Price | ₹29.80 |

| Indicative Price | ₹40.20 |

| Discount | Around 26% |

| Day High | ₹31.29 |

| Day Low | ₹28.31 |

| Closing Price | Around ₹29.51 |

| Market Cap | ₹7,001 to ₹7,166 crore |

The stock did attempt a small recovery during intraday trade and even touched ₹31.29, but the gains did not sustain. It eventually closed below expectations.

Many investors on social platforms called it a “weak debut.” Some were surprised because of Unilever backing. But others pointed out that the ice cream business is capital intensive and seasonal. That naturally makes short-term investors cautious.

Why Did Kwality Wall’s Share List At A Discount?

Let us be practical here. There are multiple reasons behind the discount listing.

First is seasonality. Ice cream demand peaks in summer months. Revenue visibility in other quarters is relatively lower.

Second is margin pressure. Cold chain logistics, freezer cabinets, transportation, electricity costs. Everything adds up.

Third is competition. Amul dominates the Indian ice cream market and holds the number one position. Kwality Wall’s stands second with roughly 10 percent market share.

Fourth is valuation expectation mismatch. Some brokerages had valued the business between ₹9,500 crore to ₹11,900 crore. The listing valuation came much lower than that range.

So markets reacted cautiously. Nothing dramatic. Just typical investor behaviour.

Market Position In India’s Ice Cream Industry

Now comes the interesting part.

India’s per capita ice cream consumption is still very low compared to global averages. That means huge untapped potential.

Kwality Wall’s is present in nearly 200,000 outlets across India. Sounds big. But here is the reality. India has around 13 million FMCG outlets. That means the company still has massive room to expand.

The Indian ice cream and frozen dessert market is growing at double-digit CAGR according to industry estimates. Growth drivers include:

- Rising disposable income

- Urbanisation

- Quick commerce apps

- Changing perception of ice cream as a daily frozen snack

Kwality Wall’s is aggressively investing in distribution expansion, cold storage infrastructure, and premium product innovation. Brands like Magnum, Cornetto and Feast continue to enjoy strong consumer recall.

The company is aiming for double-digit volume growth, faster than category average.

That is a bold target. But if executed properly, it can justify long-term optimism.

Open Offer And Unilever’s Continued Involvement

Another important development is the open offer announcement.

An Unilever arm, Magnum Ice Cream Company, has announced an open offer to acquire up to 26 percent stake in the company post-listing. This move signals that global parent backing is still strong.

For investors, this provides some confidence that strategic direction and brand strength will remain aligned with global standards.

However, open offer price was reported at a discount to listing levels, which again triggered debate among investors.

Public Opinion On X And Investor Sentiment

Let us talk about real chatter happening online.

On X, investor reactions were mixed.

Some investors expressed disappointment about the 26 percent listing discount. Words like weak debut and below expectation were common.

Others took a long-term view. They highlighted India’s under-penetrated market and strong brand recall. Many called it a “long-term FMCG play” rather than a quick trading bet.

Consumer sentiment remains largely positive. Magnum is often praised for premium indulgence. Cornetto continues to enjoy nostalgic love among youngsters. However, pricing concerns do pop up occasionally, especially when compared to Amul which is seen as more affordable.

Overall sentiment summary:

- Short-term traders cautious

- Long-term investors curious but patient

- Consumers loyal but price sensitive

Growth Strategy After Demerger

Post demerger, the company can now focus fully on ice cream without competing internally for capital allocation.

Strategic focus areas include:

- Expanding distribution footprint beyond 200,000 outlets

- Increasing freezer cabinet placements

- Boosting quick commerce presence

- Launching premium innovations

- Promoting year-round consumption

The big shift is positioning ice cream as a frozen snack instead of just a summer dessert. That mindset change can significantly increase consumption frequency.

If that happens, revenue stability improves. Seasonality impact reduces gradually.

Risks Investors Should Keep In Mind

Every stock has risks. Let us be clear.

- Seasonal revenue fluctuations

- High cold chain cost

- Intense competition from Amul and regional players

- Commodity price volatility

- Premium pricing sensitivity

Market veteran opinions suggest that this may not be a stock that delivers quick short-term gains. It is more of a steady business model that needs time to scale independently.

So patience will be key.

Is Kwality Wall’s Share A Long Term Opportunity?

This depends on investor mindset. If you are looking for quick listing gains, this debut was disappointing.

If you are evaluating long-term FMCG growth in an under-penetrated category, the story looks interesting. The company has brand strength, distribution plans, and global backing.

India’s ice cream consumption trend is evolving. Quick commerce and impulse buying are growing. Urban markets are expanding fast.

The discount listing may simply reflect near-term caution rather than long-term weakness.

But as always, investors should do their own research and assess risk appetite before making decisions.

Conclusion

Kwality Wall’s share debut has created buzz across the market. A 26 percent discount listing always grabs headlines. But behind that number lies a larger story of demerger strategy, growth potential, and industry transformation.

The company now stands independently with around ₹7,000 crore market capitalisation and ambitious expansion plans. It operates in a growing category with strong consumer brands.

Short-term volatility is expected. That is normal in newly listed stocks.

The real story will unfold over the next few quarters as the company proves whether it can convert India’s low per capita consumption into consistent revenue growth.

For now, investors are watching closely. And honestly, this one is going to be interesting to track.

Related Posts :

Share This Post