Hindustan Zinc Share Price Rallies to Record High on Strong Q3 FY26 Results and Silver Surge

Hindustan Zinc Share Price Rallies to Record High on Strong Q3 FY26 Results and Silver Surge | Image Via Mint

Hindustan Zinc share price remained in strong focus on January 20, 2026, after the stock touched fresh record highs in early trade. The rally came immediately after the company announced its Q3 FY26 earnings, which turned out to be the strongest quarterly performance in its history.

Investor interest picked up sharply as rising silver prices, record revenue, and improved cost efficiency came together at the same time. Market participants tracked both the price action and management commentary closely, as Hindustan Zinc continues to benefit from a favorable commodity cycle.

Table of Contents

Key Takeaways

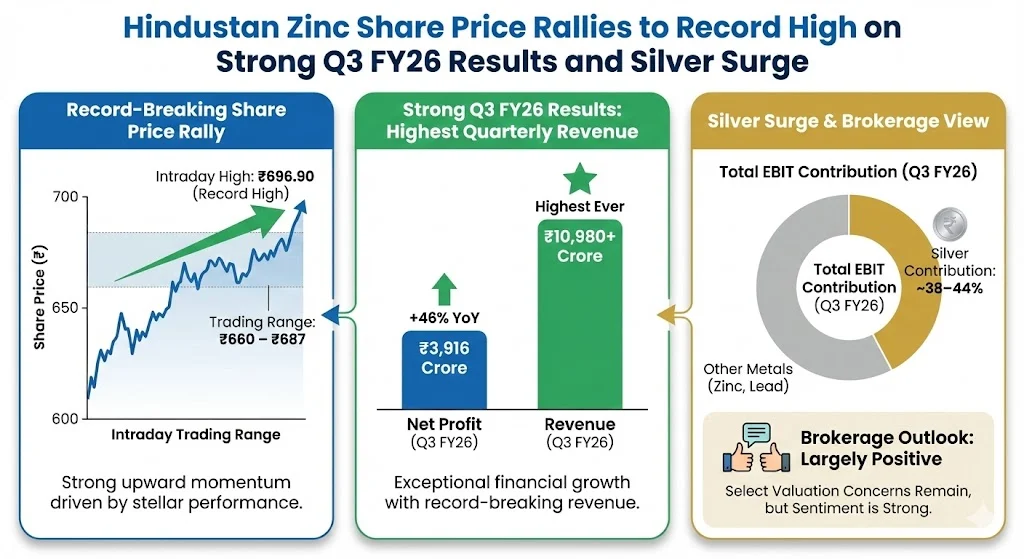

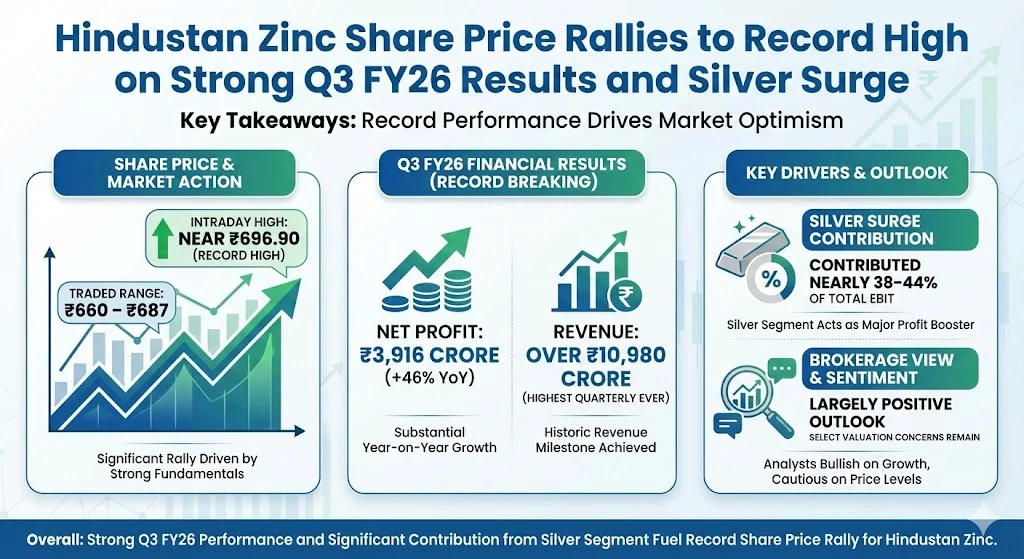

- Hindustan Zinc share price traded in the ₹660–₹687 range with intraday highs near ₹696.90

- Q3 FY26 net profit jumped 46 percent year on year to ₹3,916 crore

- Revenue crossed ₹10,980 crore, marking the highest quarterly level ever

- Silver contributed nearly 38–44 percent of total EBIT during the quarter

- Brokerages remain largely positive, with select valuation concerns

Also Read: Silver Rate Today: Silver Crosses ₹3 Lakh

Hindustan Zinc Share Price Performance Today

Hindustan Zinc shares extended their upward momentum during Tuesday’s session. The stock opened firm and moved higher as trading volumes increased, reflecting strong participation from both retail traders and institutional investors.

As of January 20, 2026, the share price traded around ₹660–₹687 during most updates. Intraday, the stock touched highs close to ₹696.90 before consolidating near the ₹685–₹686 zone. The move represented a sharp continuation of the recent rally seen over the past few weeks.

Recent price performance highlights include:

- Intraday gain of around 3 to 4 percent on strong volumes

- Weekly gains in the range of 6 to 9 percent

- Monthly rise of nearly 12 to 16 percent

- Year to date gains of about 11 to 12 percent

- One year returns exceeding 44 to 47 percent

The stock also marked a new 52 week high, rising from its March 2025 low of around ₹378. This sustained upward trend has placed Hindustan Zinc among the top performing metal stocks in early 2026.

Also Read: 8th Pay Commission Salary Hike: Latest Update, Fitment Factor Estimates and Realistic Timeline

Q3 FY26 Results Drive Market Confidence

The December quarter of FY26 proved to be a landmark period for Hindustan Zinc. The company reported its highest ever quarterly revenue and profit, driven by a mix of higher production, strong metal prices, and disciplined cost control.

Consolidated net profit for Q3 FY26 surged 46 percent year on year to ₹3,916 crore. This marked the strongest quarterly profit reported by the company so far. Revenue crossed ₹10,980 crore, registering a growth of nearly 28 percent compared to the same period last year.

EBITDA stood at ₹6,087 crore during the quarter, supported by strong operating leverage and margin expansion. EBITDA margins remained in the range of 47 to 52 percent in recent periods, placing the company among the most efficient producers in the global metals space.

A key highlight remained the reduction in zinc production cost. The cost of production declined to around $940 per tonne, the lowest level seen in several years. This improvement played a major role in boosting overall profitability during the quarter.

Role of Silver Prices in Earnings Growth

Silver prices emerged as a major catalyst behind the sharp move in Hindustan Zinc share price. The global silver market has been witnessing a strong uptrend, supported by supply constraints and rising industrial demand.

During Q3 FY26, silver contributed roughly 38 to 44 percent of the company’s total EBIT. This growing share has made Hindustan Zinc a preferred proxy for investors looking to gain exposure to the silver cycle.

Silver futures across different expiries moved higher during the same period:

| Silver Contract | Price per kg | Change |

|---|---|---|

| March expiry | ₹3,18,729 | Up ~3% |

| May expiry | ₹3,28,854 | Up ~3% |

| July expiry | ₹3,35,885 | Up ~3% |

The company is India’s largest producer of refined silver with purity levels of 99.9 percent or higher. Management has also guided for a significant ramp up in silver output, with production expected to reach around 680 tonnes in FY26 amid a global silver deficit.

Operational Strength and Cost Discipline

Operational execution remained a strong pillar of the Q3 performance. Hindustan Zinc reported record mined and refined metal production during the quarter. Improved plant availability and successful debottlenecking projects helped increase throughput across key facilities.

The company benefited from commissioning debottlenecking at the Chanderiya smelter and improved ramp up at Dariba and Debari units. These initiatives allowed the company to scale production without a sharp increase in operating costs.

Lower energy costs, process efficiencies, and improved ore grades supported the decline in cost of production. Management has indicated that further cost reductions are likely in Q4 FY26, which could help maintain margins even if metal prices fluctuate.

Public Sentiment and Trader View on Social Media ( Data Taken From X )

Public sentiment around Hindustan Zinc share price has remained strongly positive across social media platforms. Traders and long term investors have highlighted the stock’s sharp reaction after the earnings announcement and its strong linkage to silver prices.

Recent posts pointed to quick gains such as moves from ₹670 to ₹684 within a single session. Several users shared past price trajectories, highlighting gains of over 40 percent from lower levels. Many posts described the stock as a silver driven play with strong operational backing.

Brokerage upgrades were also widely circulated. Positive reactions focused on record profits, margin expansion, and management confidence. While some users flagged valuation risks, the broader tone remained bullish, with many viewing short term dips as buying opportunities.

Brokerage Views and Analyst Targets

Brokerage opinion on Hindustan Zinc remains mixed but tilted towards the positive side. Several global and domestic firms raised targets following the Q3 earnings beat.

HSBC maintained a Buy rating and set a target price of ₹750. The brokerage cited strong earnings visibility, lower costs, and sustained strength in silver prices as key reasons. HSBC expects Q4 results to remain robust due to higher volumes and favourable commodity trends.

Jefferies also reiterated its Buy call and raised its target to ₹750. The firm highlighted the company’s benefit from rising silver and zinc prices and upgraded its FY26 to FY28 EPS estimates by 3 to 10 percent. Jefferies expects strong EPS growth in FY27, supported by operational efficiency.

On the cautious side, Citi retained a Sell rating with a target of ₹585. The firm pointed to valuation concerns despite acknowledging the strong EBITDA growth. Nuvama maintained a Reduce rating with a target of ₹591, citing expensive valuations at around 11x FY28 EV to EBITDA.

Despite these differing views, the majority of market participants continue to focus on earnings momentum and commodity tailwinds.

Valuation & Long Term Outlook

At current levels, Hindustan Zinc trades at a premium to its historical averages. Valuation metrics such as PE and EV to EBITDA reflect the market’s expectations of sustained earnings growth.

The company is currently valued at around 24 to 26 times PE, with EV to EBITDA estimates in the range of 9 to 11 times for forward years. While this has raised caution among some analysts, others argue that the premium is justified due to the rising contribution from silver and consistent free cash flow generation.

Long term growth drivers include expansion projects, tailings reprocessing, and a strong push towards renewable energy. Management aims to increase renewable energy usage to nearly 70 percent by FY28, which could further reduce costs and improve sustainability metrics.

Conclusion On Hindustan Zinc Share Price

Hindustan Zinc share price has emerged as one of the standout performers in the metals sector in early 2026. Record Q3 FY26 results, strong silver prices, and disciplined cost management have combined to drive the stock to new highs.

While valuation concerns remain for some investors, the company’s earnings momentum, low cost structure, and growing exposure to silver continue to support positive sentiment. As long as commodity prices remain supportive and execution stays strong, Hindustan Zinc is likely to remain in focus for both traders and long term market participants.

Also Read: Income Tax Refund News January 2026: Why Lakhs of Taxpayers Are Still Waiting

Tags: Hindustan Zinc, Hindustan Zinc share price, metal stocks, silver prices, Q3 results, stock market news

Related Posts :

Share This Post