Master These 15 Unbeatable Rules To Be Undefeated In Investing & Budgeting

Master These 15 Unbeatable Rules To Be Undefeated In Investing & Budgeting

Master these rules to be undefeated in investing and budgeting because I have seen too many people lose their hard-earned money by ignoring basic principles.

After spending years in the market and managing my own portfolio through bull runs and crashes, I can tell you that success is not about complicated strategies. It is about following time-tested rules that legendary investors have proven over decades.

Warren Buffett just retired in December 2025 and the entire investing world is talking about his principles again.

Why? Because these rules work regardless of market conditions. Whether you are investing your first 10000 rupees or managing crores, these fundamental guidelines will protect your capital and help you build real wealth.

I remember when I started investing without any rules. I chased hot stocks, overtrade constantly and watched my money disappear. Then I discovered these principles and everything changed. My portfolio stabilized, my returns improved and I finally understood what investing actually means.

Today I am sharing 15 powerful rules that cover everything from stock selection to retirement planning. These are not theoretical concepts. I use them daily and they have transformed how I approach money.

Table of Contents

KEY TAKEAWAYS:

- Warren Buffett’s two cardinal rules focus on capital preservation above everything else

- Concentration strategies like the 20-slot punch card rule beat mindless diversification

- Value investing formulas like Graham Number help identify undervalued opportunities

- Growth metrics like PEG ratio balance valuation with future potential

- Retirement rules like 4% withdrawal rate need adjustment for current market conditions

- Compounding calculators like Rule of 72 simplify long-term planning

- Budget allocation through 50/30/20 rule creates financial stability

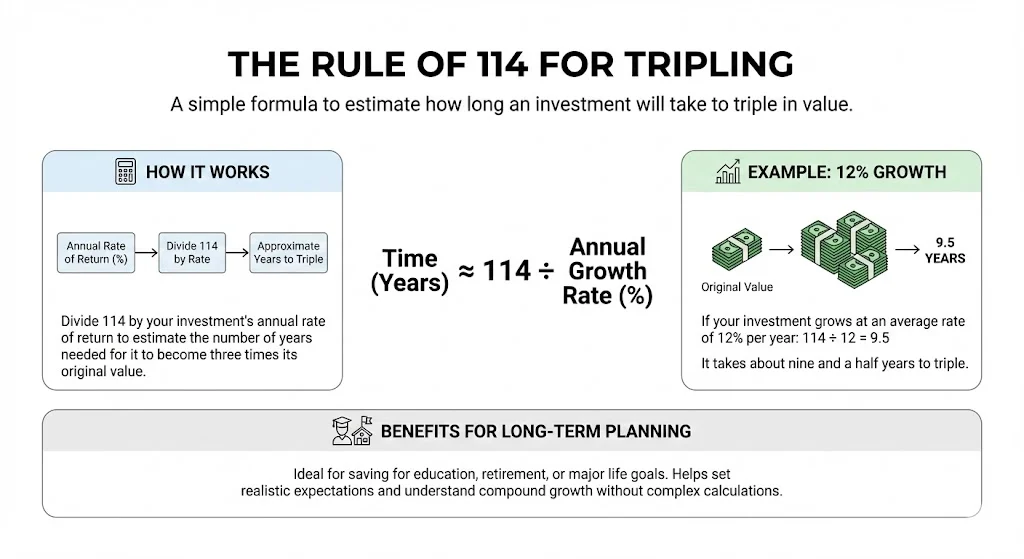

The Rule of 114 for Tripling

The Rule of 114 is a simple financial formula used to estimate how long an investment will take to triple in value. It works in a similar way to the Rule of 72, but instead of showing when money will double, it focuses on tripling growth.

To use this rule, divide 114 by the annual rate of return on your investment. The result gives an approximate number of years needed for your money to become three times its original value.

For example, if your investment grows at an average rate of 12 percent per year, dividing 114 by 12 gives 9.5. This means your investment is expected to triple in about nine and a half years.

The Rule of 114 is especially useful for long term financial planning such as saving for children’s education, retirement, or major life goals. It helps investors set realistic expectations and understand the power of compound growth over time without using complex calculations.

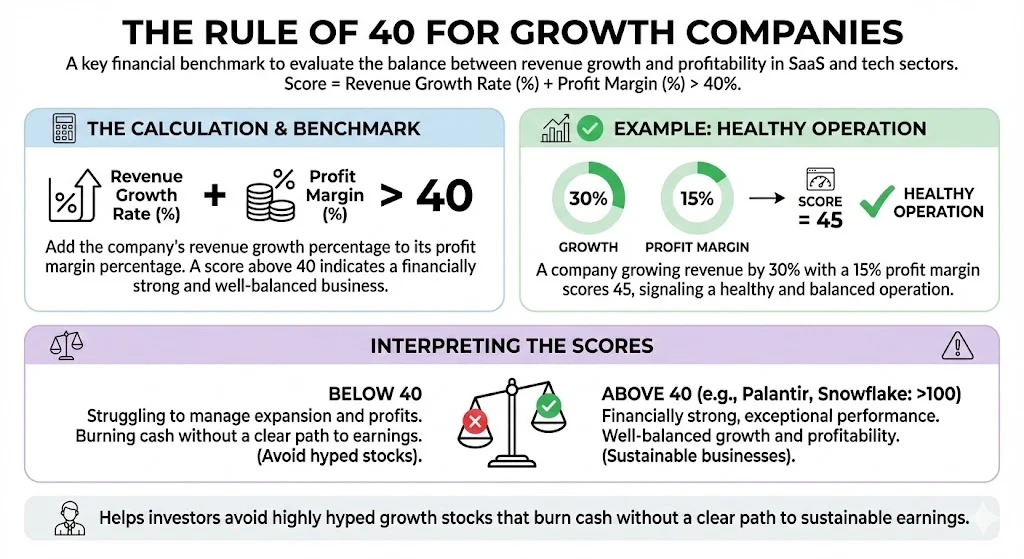

The Rule of 40 for Growth Companies

The Rule of 40 is a popular financial benchmark used to evaluate the health of growth companies, especially in SaaS and technology sectors. It combines two key factors that define business strength which are revenue growth rate and profit margin.

To calculate it, simply add the company’s revenue growth percentage to its profit margin percentage. If the total is above 40, the business is considered financially strong and well balanced between growth and profitability.

For example, if a company grows revenue by 30 percent and has a profit margin of 15 percent, its Rule of 40 score becomes 45, which signals a healthy operation. Companies like Palantir and Snowflake score above 100, showing exceptional performance and strong business quality.

Firms that fall below 40 often struggle to manage expansion while maintaining profits. This rule helps investors avoid highly hyped growth stocks that burn cash without a clear path to sustainable earnings.

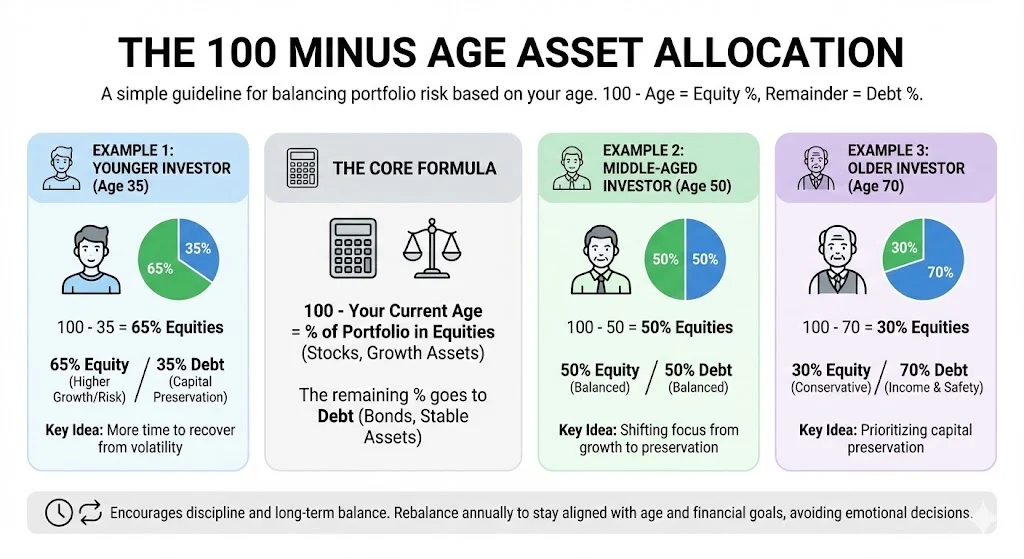

The 100 Minus Age Asset Allocation

The 100 Minus Age rule is a simple guideline for deciding how much of your portfolio should be invested in equities and how much should be in safer assets like debt or bonds.

To use this rule, subtract your current age from 100. The result gives the percentage of your investments that should be allocated to equities, while the remaining portion goes into debt instruments.

For example, at age 35, subtracting 35 from 100 gives 65. This means 65 percent of the portfolio stays in equities and 35 percent in debt.

The idea behind this rule is that younger investors can handle market volatility because they have more time to recover from losses. As retirement gets closer, preserving capital becomes more important than chasing high returns, so the share of debt gradually increases.

This method encourages discipline and long term balance. Rebalancing the portfolio every year using this formula helps investors avoid emotional decisions during market ups and downs and keeps risk aligned with age and financial goals.

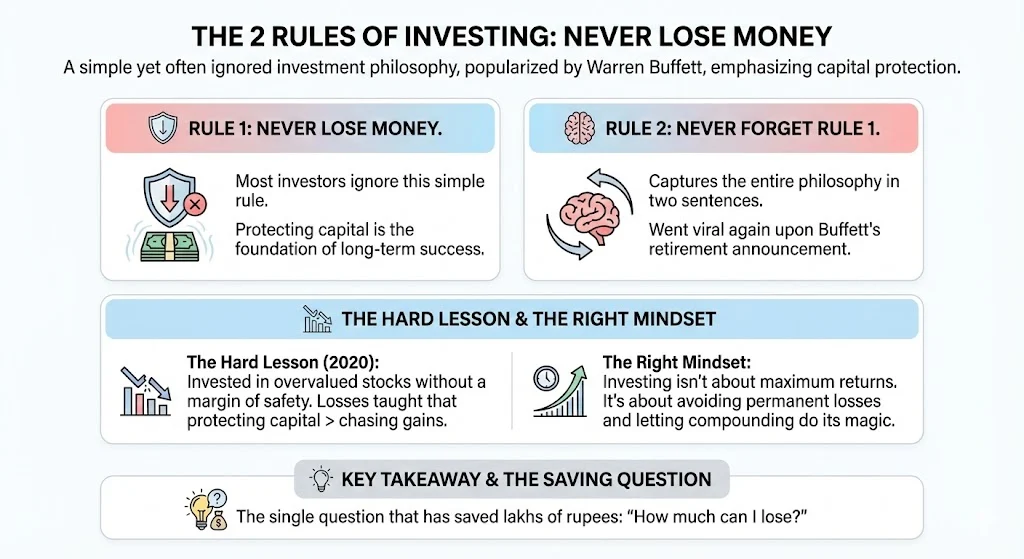

The 2 Rules of Investing: Never Lose Money

Rule number one is never lose money. Rule number two is never forget rule number one. I know this sounds simple but most investors ignore it completely. When Buffett announced his retirement, this rule went viral again because it captures his entire philosophy in two sentences.

I learned this lesson the hard way in 2020 when I invested heavily in overvalued stocks without any margin of safety. The losses taught me that protecting capital matters more than chasing gains. Now before every investment I ask myself how much can I lose. This single question has saved me lakhs of rupees.

People think investing is about making maximum returns. Wrong. It is about avoiding permanent losses while letting compounding do its magic over time. The difference is massive.

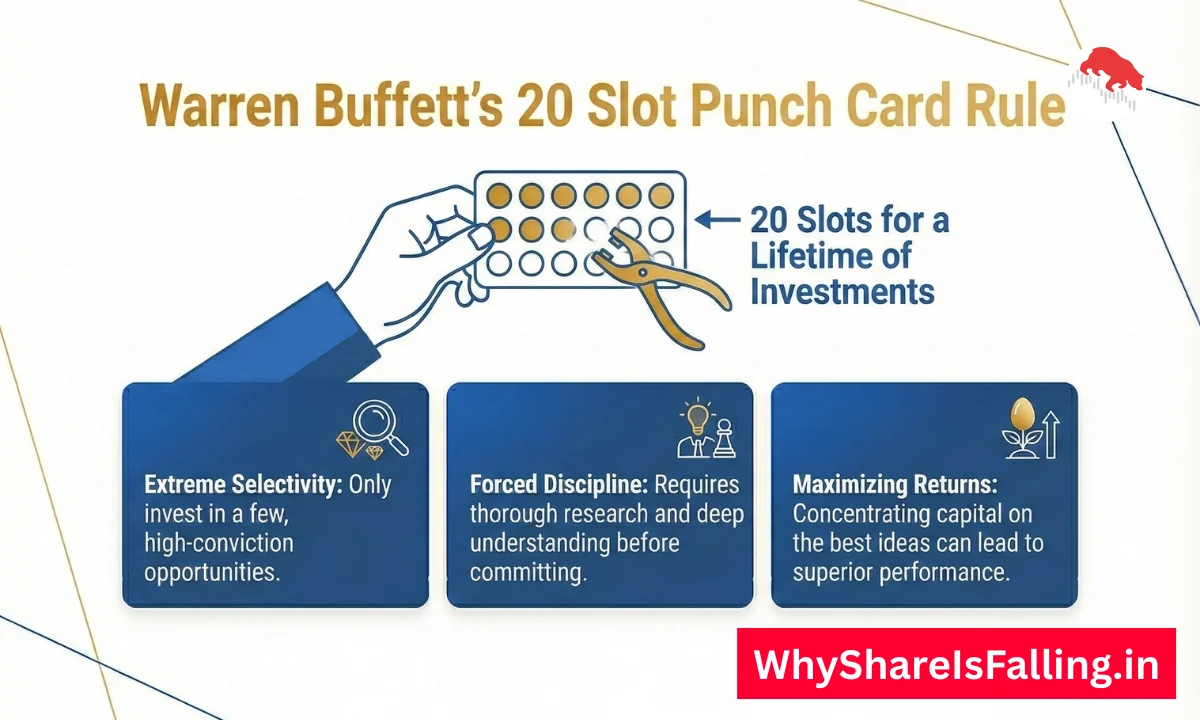

The 20-Slot Punch Card Rule

Imagine you only get 20 investment decisions in your entire life. Would you waste them on random stock tips or mediocre companies. This is Buffett’s punch card rule and it changed how I invest forever.

I used to trade constantly thinking more activity equals more money. My portfolio had 30 stocks and I knew nothing about most of them. Then I applied this rule. I cut down to 8 high conviction holdings that I researched deeply. My returns doubled because I focused only on my best ideas.

This rule forces you to be selective. You study businesses thoroughly, wait for great prices and hold for years. Fewer bets but better bets. That is how wealth compounds.

Read More: Warren Buffett’s 20 Slot Punch Card Rule: A Simple Path To Smarter Investing

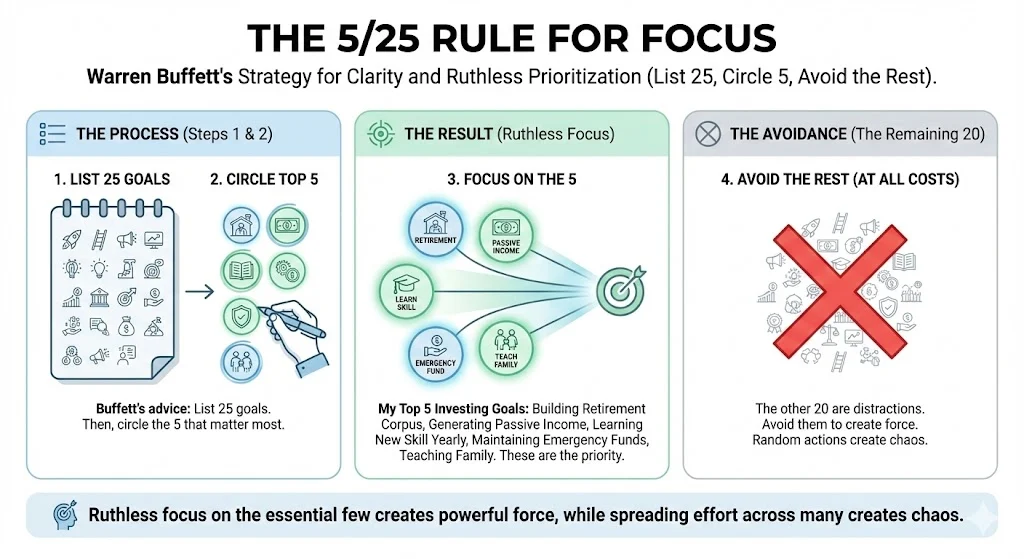

The 5/25 Rule for Focus

Buffett told his pilot to list 25 career goals, circle the top 5 and avoid the remaining 20 at all costs. I applied this to investing and life decisions. The clarity is unbelievable.

My top 5 investing goals include building a retirement corpus, generating passive income, learning one new analysis skill yearly, maintaining emergency funds and teaching my family about money. Everything else is distraction. This ruthless focus creates force while random actions create chaos.

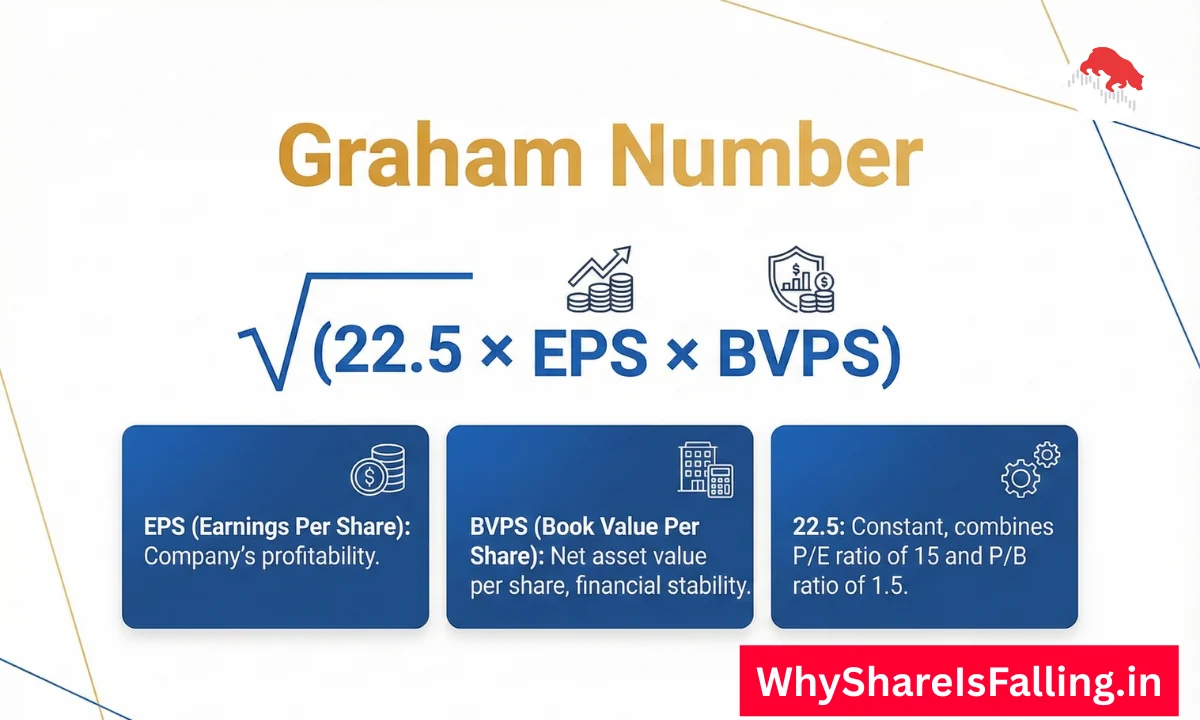

The Graham Number Formula

Benjamin Graham’s formula calculates intrinsic value using earnings and book value. The number is 22.5 multiplied by square root of EPS times BVPS. When stock price falls below this, you have found a potential bargain.

I use this for screening undervalued companies especially in manufacturing and auto ancillary sectors. Last year I found several stocks trading 60-70% below their Graham Number. Some of them gave me 40% returns as market recognized their true worth. The margin of safety this formula provides is incredible for conservative investors.

Read More: The 15 x 1.5 Rule: Understanding The Graham Number In Value Investing

The PEG Ratio Sweet Spot

Peter Lynch taught me to look beyond PE ratios. PEG ratio divides PE by growth rate and ideally you want it below 1.0. This balances valuation with future potential.

I use PEG for growth stocks where high PE seems scary at first. A company with 30 PE growing at 35% annually has PEG of 0.85 which signals undervalued growth. This helped me stay invested in quality tech companies that seemed expensive but were actually mispriced. PEG works brilliantly when combined with other metrics.

The 5-Stock Concentrated Portfolio

Diversification is protection against ignorance. If you know what you are doing, concentration builds serious wealth. I maintain a core portfolio of 5-7 stocks that I understand deeply.

Each position gets 15-20% allocation and I track these businesses like I own them completely. This approach is volatile short term but the long term returns crush over-diversified portfolios. You need conviction and research but the rewards justify the effort. My concentrated holdings outperformed my diversified experiments by significant margins.

Hunting for Ten-Baggers

Peter Lynch coined this term for stocks that return 10 times your investment. I actively hunt for these in small and mid cap space where growth potential is enormous.

The key is finding companies in their second or third inning not ninth. I look for scalable business models, growing markets and competent management. Ten baggers require patience because they take 5-10 years to materialize. My portfolio has two potential ten baggers that I accumulated at attractive prices. The pain of waiting now will create legendary returns later.

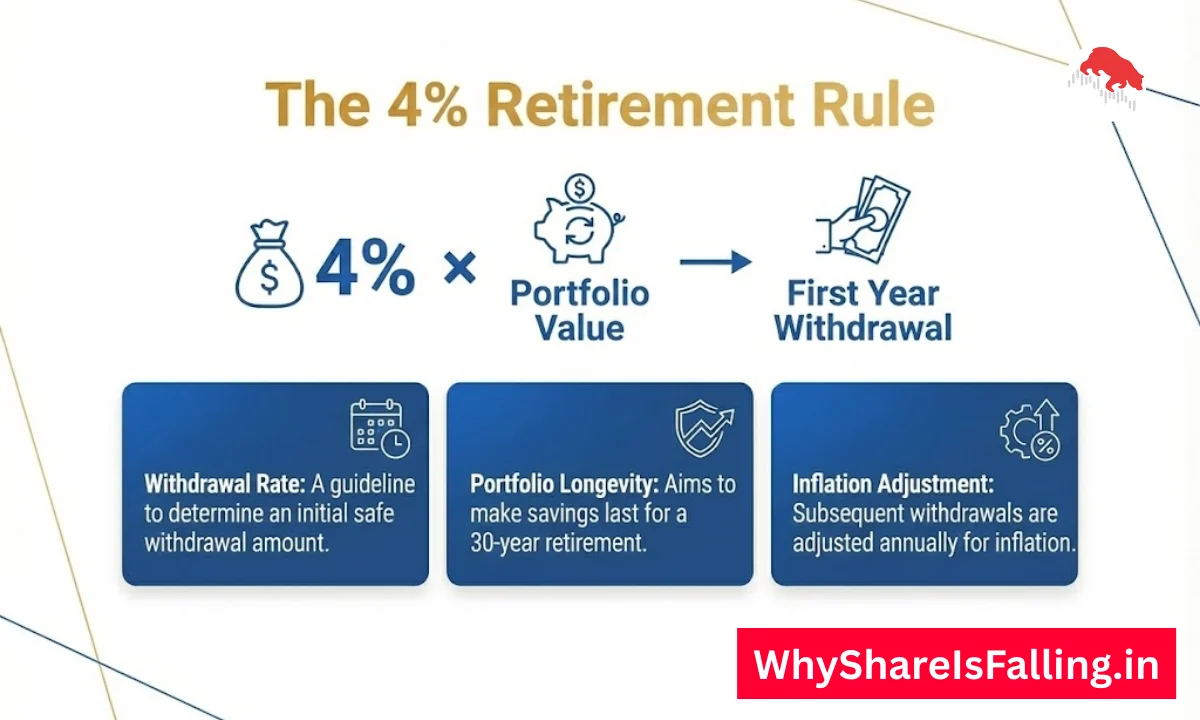

The 4% Retirement Rule

William Bengen’s research showed you can withdraw 4% of your retirement corpus initially and adjust for inflation. This should last 30 years historically. I plan my retirement using this as baseline.

However 2026 conditions demand caution. With high valuations and inflation concerns, I use 3.5-3.8% to be conservative. Starting with lower withdrawal rate during poor market sequences protects your corpus. Bengen himself updated his research suggesting 4.7-5.5% works with diversified assets but I prefer being safe than sorry with retirement money.

The 50/30/20 Budget Rule

This allocation changed my financial life completely. I dedicate 50% of income to needs like rent, food and utilities. 30% goes to wants like entertainment and dining. 20% gets invested religiously.

When I started following this, my savings rate jumped from 8% to 20% immediately. The clarity of having defined buckets eliminates guilt about spending and ensures consistent investing. I automate the 20% investment on salary day so temptation never interferes. This rule works for any income level if you are honest about needs versus wants.

Read More: The 50-30-20 Rule Re-engineered: Smart Budgeting Made Simple

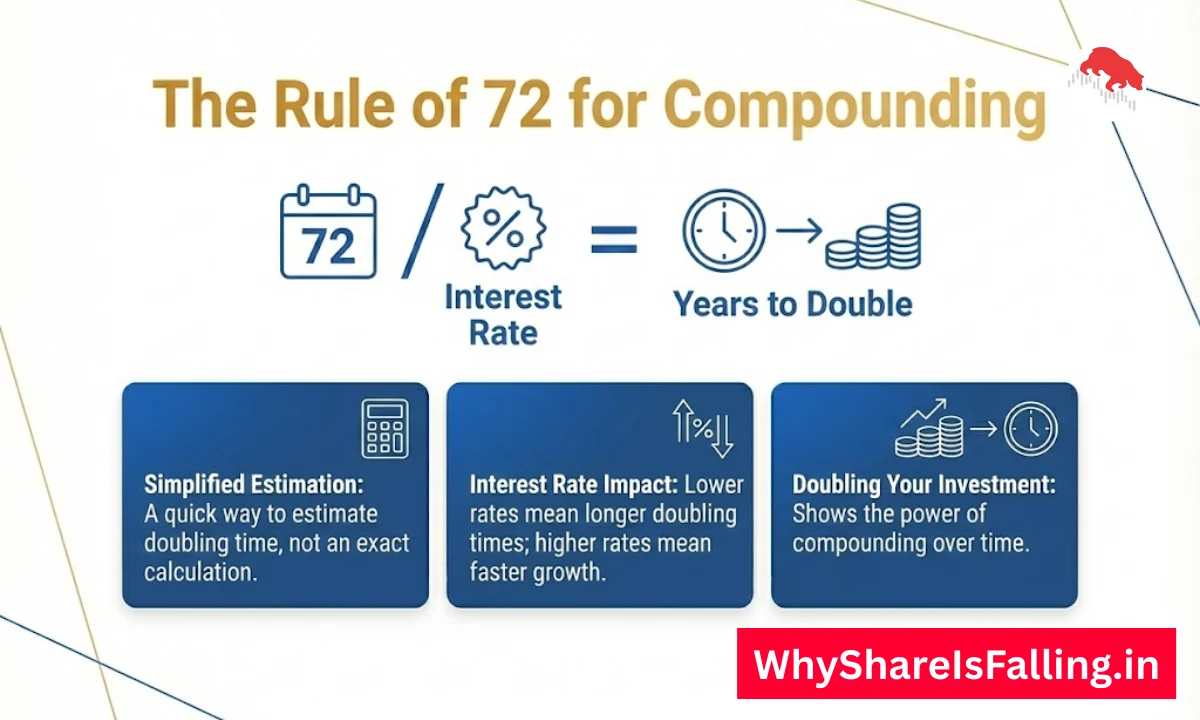

The Rule of 72 for Compounding

Divide 72 by your annual return percentage to know doubling time. At 12% returns, my money doubles every 6 years. This simple calculation keeps me focused on long term compounding.

I use this to show family members why starting early matters exponentially. Someone starting at 25 with 10000 monthly at 12% will have nearly 3.5 crores by 55. Starting at 35 with same amount gives only 1 crore. The difference is all about number of doubling periods. Rule of 72 makes this tangible instantly.

The Rule of 20 for Market Valuation

Add market PE ratio and inflation rate. Below 20 signals undervalued market, above suggests overvaluation. I use this to adjust my equity allocation tactically.

Currently with elevated valuations, this rule suggests caution. I am not selling everything but I am selective about new purchases and maintaining higher cash reserves. Market timing is impossible but valuations matter over long term.

Read More: The Rule Of 20 In Stock Valuation: Earnings vs Growth

Following these rules transformed my investing from gambling to systematic wealth creation. I have seen my portfolio survive crashes, generate consistent returns and compound steadily. The best part is these principles work regardless of market fashion or economic conditions.

Start with 2-3 rules that resonate most. Master them through practice. Add more as your understanding deepens. Investing success is not about knowing everything. It is about following proven rules with discipline and patience.

TAGS: investing rules, budgeting tips, Warren Buffett principles, retirement planning, stock market strategy, personal finance management, wealth building techniques

Related Posts :

Share This Post