The 40 30 20 10 Rule: A Modern Budget Strategy For Rising Costs

The 40 30 20 10 Rule: A Modern Budget Strategy For Rising Costs

Managing money has become more complex in recent years as the cost of living rises and incomes do not always grow at the same pace. People want a budgeting method that is simple, flexible, and realistic in high inflation environments. This is where the 40 30 20 10 rule has started gaining strong attention among personal finance planners and everyday earners.

Table of Contents

Key Takeaways On 40 30 20 10 Rule

- The 40 30 20 10 rule divides after tax income into four spending categories

- It helps balance needs, lifestyle spending, long term investments, and emergency funds

- It is seen as a modern upgrade to the 50 30 20 rule

- The method suits middle income earners in high cost cities

- It focuses on financial discipline without removing lifestyle comfort

The rule follows the same foundation as popular percentage based frameworks like the 50 30 20 rule but adds more structure. It is designed to help maintain liquidity, support long term investing, and still allow guilt free spending on wants.

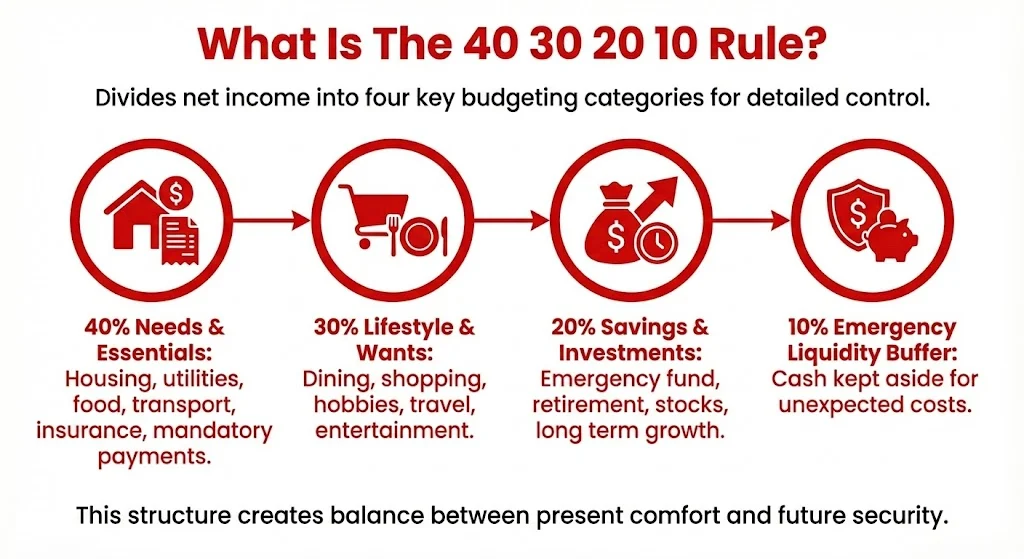

What Is The 40 30 20 10 Rule?

The 40 30 20 10 rule divides your net income into four key budgeting categories. This split gives more detailed control over where your money flows each month.

The Income Split Works Like This

| Category | Percentage | Meaning |

|---|---|---|

| Needs and Essentials | 40% | Housing, utilities, food, transport, insurance, mandatory payments |

| Lifestyle and Wants | 30% | Dining, shopping, hobbies, travel, entertainment |

| Savings and Investments | 20% | Emergency fund, retirement, stocks, long term growth |

| Emergency Liquidity Buffer | 10% | Cash kept aside for unexpected costs |

This structure creates balance between present comfort and future security. It caps essential spending at 40 percent which encourages mindful living. At the same time, lifestyle spending still has enough space at 30 percent so the plan does not feel restrictive.

Also Read: 10 5 3 Rule Of Investment: A Simple Guide For Realistic Returns

Why This Rule Became Trending In 2025 And 2026

Financial conversations in 2025 and early 2026 highlighted one big reality. In metro locations like Mumbai, Delhi, New York and other high cost cities, traditional budgeting percentages often fail in real life. Housing alone can consume 30 to 40 percent or more of monthly pay.

The 40 30 20 10 rule reacts to this environment. It introduces a dedicated emergency liquidity section of 10 percent. This prevents people from touching investment money when a sudden expense appears. That layer of protection has made the rule stand out.

Financial blogs and tools began listing this rule as an alternative to the 50 30 20 split. It is now seen as a smarter method for people seeking financial independence while still living a balanced lifestyle.

How People React To The Rule On Social Media

Mentions of the exact term “40 30 20 10 rule” are still niche but positive. Users on X (formerly Twitter) describe it as realistic, flexible, and disciplined without feeling harsh.

Some people share their personal version of the rule. One user divided spending as 40 percent needs, 30 percent wants, 20 percent investments, and 10 percent financial runway. Others adapt it based on debt payments or entertainment priorities. The core idea stays the same. Structure plus flexibility.

There is also clear support for the dedicated emergency runway. This 10 percent liquidity fund is seen as smart planning in uncertain economies.

How The Rule Improves Financial Discipline

People like this method because it helps achieve several important financial goals at once. It builds savings, controls lifestyle spending, and avoids panic during emergencies.

Here is the only listicle in this article.

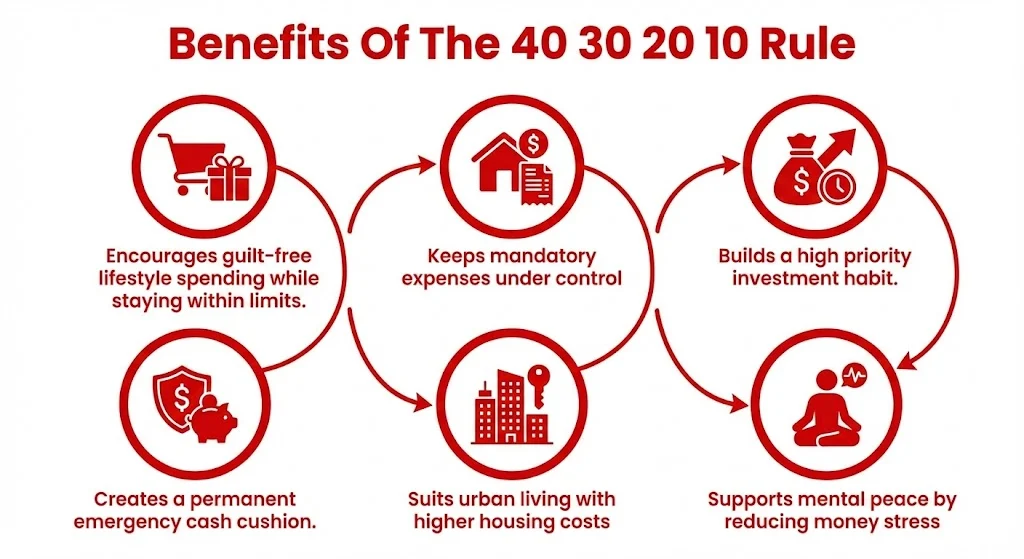

Benefits Of The 40 30 20 10 Rule

- It encourages guilt free lifestyle spending while staying within limits

- It keeps mandatory expenses under control

- It builds a high priority investment habit

- It creates a permanent emergency cash cushion

- It suits urban living with higher housing costs

- It supports mental peace by reducing money stress

This balance is one reason the rule is rising in popularity among middle income earners and young professionals.

Example Of How The Rule Works

Assume your monthly take home income is 1,00,000.

Your budget would look like this:

- 40,000 for needs

- 30,000 for lifestyle spending

- 20,000 for savings and investments

- 10,000 for emergency liquidity

The goal is clarity. Every rupee has a purpose. You are not guessing where your income disappears.

Comparison With The 50 30 20 Rule

The 50 30 20 method keeps 50 percent for needs, 30 percent for wants, and 20 percent for savings. However, many people today see their needs crossing 50 percent or prefer higher savings protection.

The 40 30 20 10 rule:

- Reduces dependency on credit cards

- Builds long term wealth through compounding

- Keeps cash buffer separate from investments

It is less rigid than zero based budgeting but more structured than pay yourself first models.

Who Should Use This Budget Rule?

This budgeting style is best for people who:

- Live in rising cost cities

- Want to save seriously without cutting lifestyle

- Prefer structure over extreme frugality

- Want dedicated emergency protection

It may suit professionals, salaried employees, entrepreneurs, and disciplined savers.

Realistic Concerns And Limitations

Some critics call percentage based rules arbitrary. Others say the model may not suit very low income households or heavy debt cases. Still, the method remains flexible. People adjust the numbers slightly while keeping the structure intact.

The aim is guidance, not pressure.

Why The Rule Reflects Today’s Economy

The last few years brought high inflation, rent spikes, job uncertainty, and a rise in remote work. People now want budgeting systems that feel resilient and practical. The 40 30 20 10 method mirrors this mindset.

It supports:

- Preparedness

- Stability

- Flexibility

- Growth

This is why interest continues to grow across financial communities worldwide.

Final Thoughts On 40 30 20 10 Rule

The 40 30 20 10 rule is more than a budgeting trend. It is a structured mindset for modern money management. It separates spending into clear priority groups. It protects your future wealth. It also allows financial breathing room so your life does not feel restricted.

If you want a budget framework that balances security and lifestyle comfort, this method can be a strong starting point. Adjust it slowly based on your income, city, and responsibilities. The key idea is consistency and clarity.

Tags: budgeting rule, personal finance planning, savings and investments, cost of living, emergency fund, financial discipline

Related Posts :

Share This Post