NHPC is one of the India’s largest hydropower generation company. It is also backed by the Government India. It was established in 1975 and is headquartered in Faridabad, Haryana.

The company mainly develops and operates hydroelectric power projects. It has also expanded into solar power, wind energy and pumped storage projects. NHPC plays a key role in India’s clean energy mission. It operates more than 7,000 MW capacity and has over 8,500 MW under construction.

In the last five years the company has shown stable revenue. However profit growth has been volatile due to hydrology issues and rising interest cost.

The stock is currently trading around ₹75–76 in February 2026. Promoter holding remains strong as Government of India holds more than 67 percent stake.

This provides stability but also limits aggressive private style expansion. Recent Q3 FY26 results showed pressure on margins. Operating margin declined sharply due to higher finance cost. Still the long term renewable theme supports NHPC.

In this blog post we are going to see the Share Price Target of the NHPC from 2026-2050 and try to see how much returns can you expect from this in long term. We are also going to explore the vital numeric data related to the NHPC so that you can get more clear understanding for the future growth of NHPC

Table of Contents

NHPC Share Price Target 2026

| Year | Target 1 | Target 2 | Target 3 |

|---|---|---|---|

| 2026 | ₹85 | ₹95 | ₹110 |

In 2026 NHPC may see recovery driven by project commissioning. Unit 2 of the 2,000 MW Subansiri Lower project has already synchronized. More units coming online will increase generation. The board has approved ₹5,703 crore investment for Uri-I Stage-II and Dulhasti Stage-II in Jammu & Kashmir. These two projects will add around 500 MW capacity.

Government policy also supports hydro sector. Draft National Electricity Policy 2026 focuses on pumped storage and hydro expansion. If execution remains smooth and hydrology remains normal then earnings visibility can improve. However high debt and arbitration payout of ₹227 crore to HCC remain short term concerns. Overall 2026 could be a recovery year.

NHPC Share Price Target 2027

| Year | Target 1 | Target 2 | Target 3 |

|---|---|---|---|

| 2027 | ₹98 | ₹115 | ₹130 |

By 2027 NHPC may benefit from full year contribution of new projects. Capacity addition improves revenue base. The company is also raising around ₹2,000 crore through bonds. This will support capital expenditure but it will also increase finance cost.

AI and sustainability initiatives are positive signs. NHPC is using AI and ML for predictive maintenance and flood monitoring. It is working with ISRO and NRSC for glacial lake monitoring. These steps improve operational safety in Himalayan projects. If margins stabilize and debt is managed properly then investor confidence may improve in 2027.

NHPC Share Price Target 2028

| Year | Target 1 | Target 2 | Target 3 |

|---|---|---|---|

| 2028 | ₹120 | ₹140 | ₹160 |

In 2028 pumped storage projects can become important. India needs storage to balance solar and wind power. Hydro and pumped storage are reliable for peak demand. NHPC is well positioned in this segment.

Transmission expansion plan worth ₹6.4 trillion to evacuate hydro power from North East region is another long term trigger. If government executes this plan on time then hydro producers like NHPC will benefit. Execution risk remains due to geological challenges in hilly terrain. But long term demand for clean baseload power remains strong.

NHPC Share Price Target 2029

| Year | Target 1 | Target 2 | Target 3 |

|---|---|---|---|

| 2029 | ₹150 | ₹170 | ₹190 |

By 2029 many under construction projects such as Pakal Dul and Kiru are expected to progress further. Faster commissioning will increase regulated tariff income. Hydro projects provide long term PPAs which ensure stable cash flow.

However investors must track debt to equity ratio. Hydro projects require large upfront investment. If revenue growth remains low then return ratios may stay under pressure. So 2029 outlook depends on execution and interest cost control.

NHPC Share Price Target 2030

| Year | Target 1 | Target 2 | Target 3 |

|---|---|---|---|

| 2030 | ₹180 | ₹210 | ₹240 |

By 2030 India’s renewable capacity target will be much higher. Hydro will play a balancing role in grid stability. NHPC’s diversified presence in hydro, solar, and pumped storage can provide growth.

If Subansiri Lower fully operates at 2,000 MW then revenue base will expand meaningfully. Long term hydro assets generate stable cash for decades. If ROE improves from current low levels then valuation multiple can expand. 2030 can reflect structural growth if debt and margin issues are resolved.

NHPC Share Price Target 2040

| Year | Target 1 | Target 2 | Target 3 |

|---|---|---|---|

| 2040 | ₹320 | ₹360 | ₹400 |

By 2040 India aims for deep decarbonization. Hydro will be critical for grid balancing. NHPC may operate a much larger renewable portfolio including pumped hydro storage. Long life assets provide predictable income.

Technology upgrades and sediment management solutions will improve plant life. The Salal reservoir sediment issue shows challenges in older plants. Better water management and modernization will be required. If NHPC adapts well then it can remain a strong PSU in renewable sector.

NHPC Share Price Target 2050

| Year | Target 1 | Target 2 | Target 3 |

|---|---|---|---|

| 2050 | ₹550 | ₹620 | ₹700 |

By 2050 India targets net zero goals. Clean energy companies may command premium valuations. NHPC has strategic importance due to water based generation. Long term assets can deliver compounding returns if managed efficiently.

However climate change can also impact hydrology patterns. So water flow risk remains a factor. Investors with long term horizon may see NHPC as a stable compounding PSU rather than a high growth private player.

Should I Buy NHPC Share?

NHPC focuses on hydro and renewable expansion. It is investing in new projects like Uri and Dulhasti expansion. It is also adopting AI for safety and efficiency. Government support is strong. Sector outlook is positive.

But profit volatility and high debt are risks. The company faced arbitration payout and margin pressure in FY26. So investors should track quarterly results. Do your own research before investing. Always keep risk in mind.

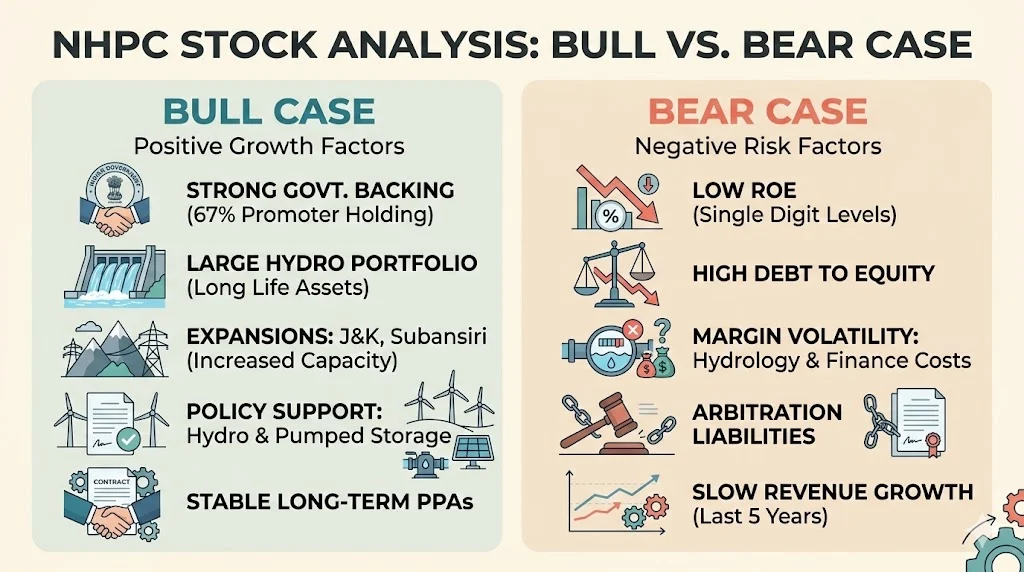

Is NHPC Stock Good To Buy? (Bull Case & Bear Case)

Bull Case

- Strong government backing with 67 percent promoter holding

- Large hydro portfolio with long life assets

- Subansiri and J&K expansions increase capacity

- Positive policy support for hydro and pumped storage

- Stable long term PPAs

Bear Case

- Low ROE around single digit levels

- High debt to equity

- Margin volatility due to hydrology and finance cost

- Arbitration liabilities

- Slow revenue growth in last five years

Key Financial Data of NHPC

| Particular | Data | Remarks |

|---|---|---|

| Promoter Holding | ~67% | Strong government control |

| Revenue Growth (5Y) | ~0.73% | Very low growth |

| Profit Growth | Volatile | Impacted by finance cost |

| ROE | ~9% | Below ideal 15% level |

| Debt to Equity | Around 1+ | Moderate to high |

| Net Profit Margin | Sharp decline in FY26 Q3 | Margin pressure visible |

| Market Cap | ~₹76,000–99,000 Cr | Large cap PSU |

| Dividend Yield | Moderate | PSU dividend support |

Detailed Analysis

Promoter holding above 60 percent is positive for stability. It shows government confidence. But it also limits aggressive risk taking.

Revenue growth of 0.73 percent over five years is weak. It means company needs new capacity to boost top line. Profit growth has been unstable. Q3 FY26 showed sharp drop due to higher interest and lower margin.

ROE around 9 percent is below ideal benchmark of 15 percent. This means capital efficiency is low. Debt to equity above 1 shows leverage is significant. Hydro projects are capital intensive. But high debt increases risk during weak earnings.

Net profit margin fell sharply in recent quarter. This is a concern. Market cap shows company is large cap PSU. Dividend yield is supportive for income investors.

Conclusion

NHPC Limited is a strategic renewable energy PSU. It has strong government backing and large hydro assets. Long term sector outlook is positive due to clean energy demand and storage needs. Recent project approvals and Subansiri progress are strong positives.

However short term earnings pressure and high debt are concerns. Return ratios are below ideal levels. So NHPC looks like a stable long term defensive play rather than a high growth stock.

Investors who prefer steady PSU exposure in renewable theme can consider tracking NHPC. But always analyze quarterly results, debt levels, and execution progress before making investment decisions.