Jio Financial Services Share Falling: Why The Stock Slipped 16% In 3 Months Despite Big Hype

Jio Financial Services Down ~16% over the last 3 months

If you have been tracking Jio Financial Services lately, you already know something feels off. The stock that once created massive buzz after demerger is now down nearly 16% in the last three months. From levels around ₹290 to ₹300 in early January 2026, it has corrected to around ₹262 to ₹263 by mid February 2026.

Investors are confused. Is this just normal correction or is something deeper going on? In this detailed breakdown, we will decode what is actually happening with Jio Financial Services share price, what the numbers are saying, and what public sentiment on X platform looks like right now.

Key Takeaways

- Jio Financial Services share price has fallen around 16% in 3 months

- Stock is trading near ₹262 with P/E above 100

- Revenue growth strong but profit under pressure due to rising costs

- NBFC AUM growing but margins not stable yet

- RBI norms and sector pressure impacting sentiment

- Public opinion on X largely negative with frustration visible

- Long term potential tied to Reliance ecosystem still intact

Current Stock Snapshot And Performance Trend

As of 17 February 2026, Jio Financial Services is trading around ₹262.30 on NSE. Over the past three months, returns are approximately -15.75% to -16%.

Here is a quick snapshot of key metrics:

| Metric | Value |

|---|---|

| Current Price | ₹262-₹263 |

| 52 Week High | ₹339 |

| 52 Week Low | ₹199 |

| Market Cap | ₹1,66,642 Cr |

| P/E Ratio | 103.84 |

| EPS (TTM) | 2.53 |

| 3 Month Return | -15.75% |

| 1 Month Return | Around -5.5% |

The biggest concern here is valuation. A P/E ratio above 100 means the market was pricing in aggressive future growth. When execution does not match expectations quickly, re rating happens. That is exactly what we are witnessing.

Also Read: Upcoming IPO This Month In India: February 2026 Mini IPO Season Is Here

High Valuation And Expectations Gap

One major reason behind the fall is simple. Expectations were sky high. After backing from the Reliance ecosystem and partnerships like JioBlackRock, investors assumed rapid profitability.

But here is the reality.

Revenue growth has been strong. In Q3 FY26, total income reportedly jumped more than 100% year on year to around ₹901 crore. That looks impressive.

However, net profit declined around 9% YoY to approximately ₹269 crore. Expenses surged sharply as the company moved from setup mode to active lending operations.

Market does not like profit pressure. Especially when valuation is already premium.

Transition Phase Is Costly

Jio Financial Services is not a mature NBFC yet. It is still building scale across lending, insurance, payments, and asset management.

AUM growth is visible. Assets under management reportedly reached around ₹19,049 crore. That is solid expansion. But high growth comes with higher operating cost, technology investments, compliance expenses, and risk management frameworks.

This is a transition phase. Margins are under pressure because operating expenses have increased sharply in some segments.

Retail investors expected faster bottom line visibility. That gap between expectation and delivery has hurt sentiment.

Impact Of RBI Norms And Sector Pressure

Another factor many investors are ignoring is the broader sector pressure.

RBI has tightened certain norms around broker lending and collateral requirements effective April 2026. This impacted capital market linked stocks. NBFC stocks in general have been cautious territory recently.

Foreign Institutional Investors have also reduced exposure in certain financial names in recent months. When liquidity reduces, high valuation stocks correct first.

So the 16% fall is not purely company specific. Sectoral caution is also playing a role.

Technical Signals And Momentum Weakness

From a technical perspective, the stock has been underperforming benchmark indices like Sensex and Nifty in recent months.

Short term moving averages have shown weakness. Momentum indicators signaled bearish trend in multiple sessions. Some analysts even downgraded the stock from Hold to Sell citing weak momentum and expensive valuation.

When sentiment turns negative, every small dip triggers more selling. That is exactly what we saw in January and early February.

Also Read: Cipla Share Price Falls 11% In 3 Months: Is This A Temporary Pharma Shock Or A Bigger Warning?

Public Opinion On X Platform

Now let us talk about what real people are saying.

Public sentiment on X platform has been largely negative. Many retail investors are openly frustrated. Common themes seen in discussions:

- Complaints about no visible profit growth

- Frustration over price stagnation since demerger

- Anger about overhype around partnerships

- Calls for stronger execution and faster results

Some users are even calling it one of the worst performing large cap bets in their portfolio. Strong language and emotional reactions show retail impatience.

At the same time, a smaller group believes this is a consolidation phase. They argue that long term story is intact due to Reliance ecosystem, digital reach, and distribution network.

So sentiment is divided. Short term negative. Long term hopeful.

Leadership Change And Risk Management Focus

Recently, the company announced appointment of Sandeep Khetan as Group Chief Risk Officer for a 5 year term. This signals stronger focus on risk governance and credit framework.

For a growing NBFC, robust risk management is critical. Especially when lending book expands aggressively.

This leadership change can improve internal control systems and help stabilize asset quality in future quarters. But market usually waits for visible results before reacting positively.

Why The Stock Is Still Above 52 Week Lows?

Despite correction, the stock is still well above its 52 week low near ₹199 to ₹200.

This suggests that long term investors are not fully exiting. Market cap remains strong at over ₹1.6 lakh crore. Institutional interest has not completely vanished.

There is still optionality in:

- Lending expansion

- Digital payments integration

- Insurance distribution

- Mutual fund business through JioBlackRock

- Cross selling within Reliance ecosystem

If execution improves and profit growth stabilizes, valuation compression may reverse gradually.

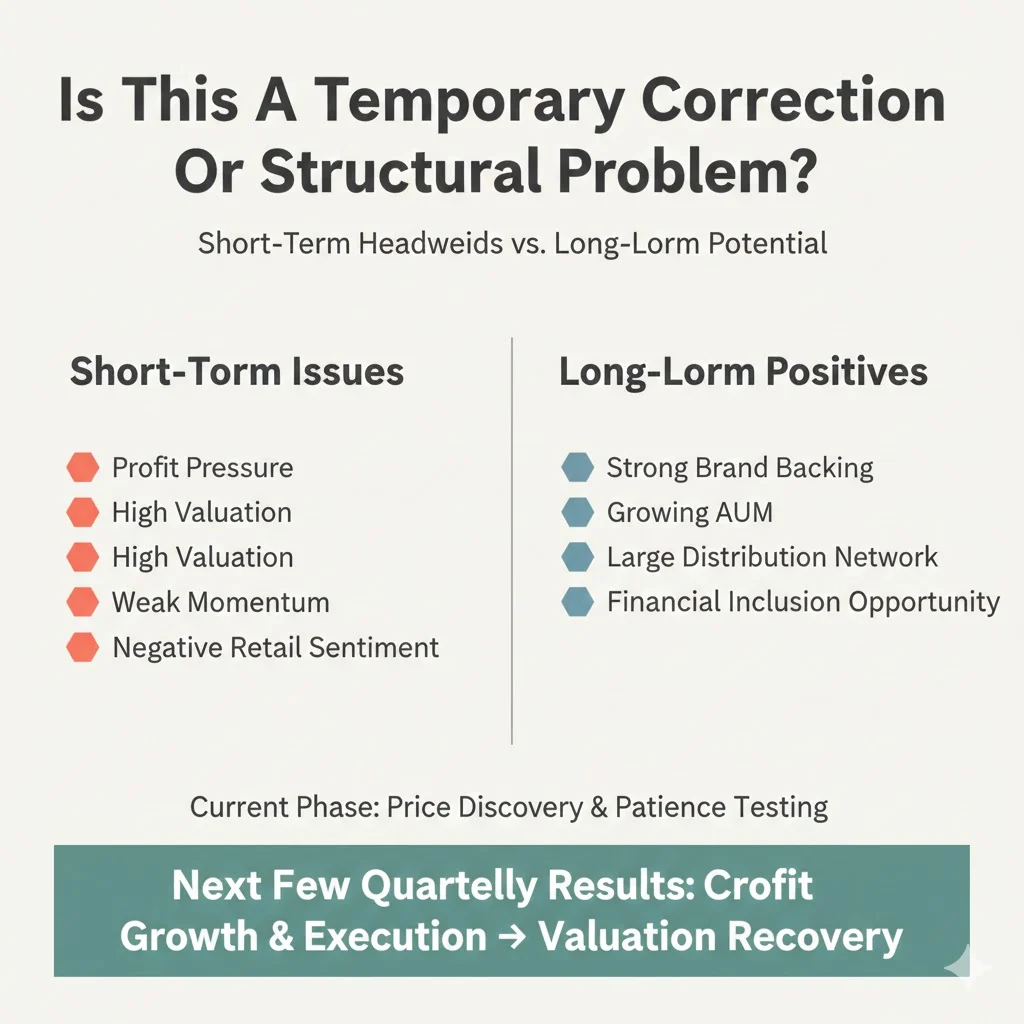

Is This A Temporary Correction Or Structural Problem?

Let us break it down clearly.

Short term issues:

- Profit pressure

- High valuation

- Weak momentum

- Negative retail sentiment

Long term positives:

- Strong brand backing

- Growing AUM

- Large distribution network

- Financial inclusion opportunity

Right now, the stock is in price discovery phase after high expectation phase. Market is testing patience of retail investors.

The next few quarterly results will be crucial. If profit growth improves and cost stabilizes, sentiment can change quickly. If margin pressure continues, consolidation may extend.

What Investors Should Watch Ahead

Instead of reacting emotionally, investors should monitor:

- Net profit trend next 2 quarters

- AUM growth sustainability

- Cost to income ratio

- Asset quality and NPA numbers

- Progress in JioBlackRock rollout

- Impact of RBI regulatory changes

Numbers will speak louder than hype.

Final Thoughts

Jio Financial Services share price down 16% in three months is not random. It reflects high valuation reset, rising costs, and sector caution.

Public opinion is currently tilted negative. Retail investors are impatient. But the company is still in expansion mode.

This phase will test conviction. Either execution improves and confidence returns. Or valuation adjusts further.

One thing is clear. Hype alone cannot sustain a P/E above 100. Only consistent profits can.

Related Posts :

Share This Post