50 30 20 Rule Of Investing: Does It Still Work In 2026?

50 30 20 Rule Of Investing: Does It Still Work In 2026?

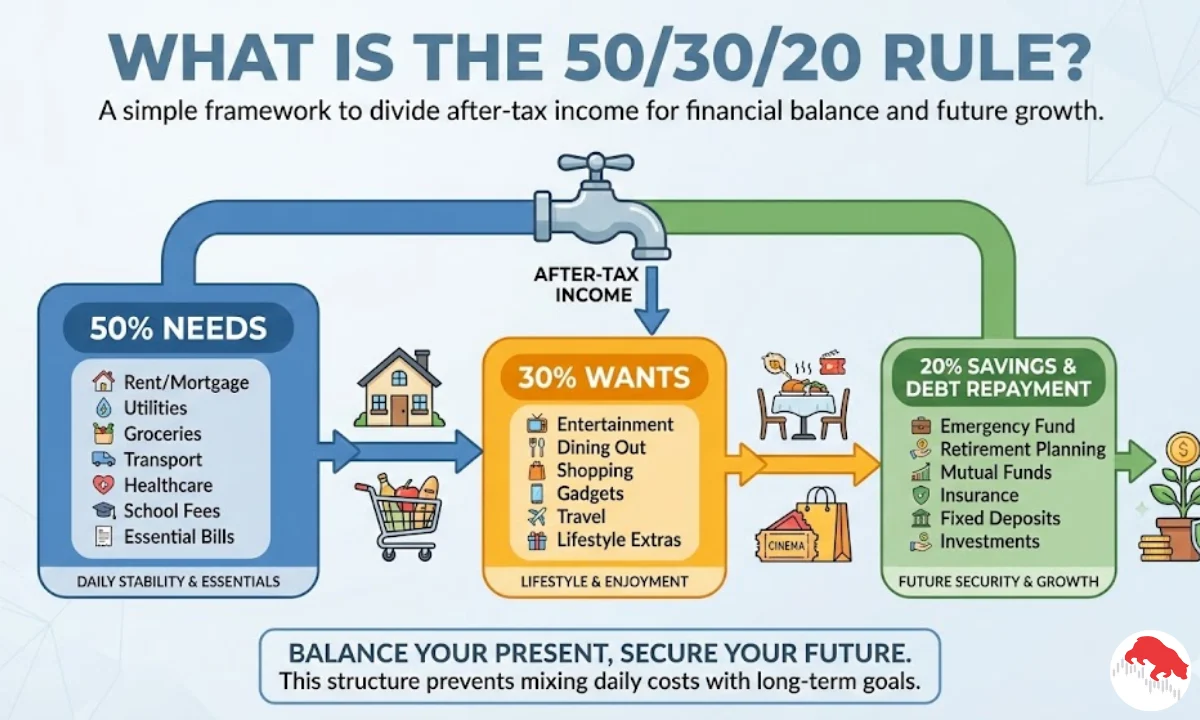

The 50 30 20 rule has remained one of the most widely shared budgeting and investing frameworks across the world. It offers a clear way to manage after tax income by dividing it into three simple parts.

Half goes to daily needs, a smaller share covers lifestyle spending, and the rest supports savings and investments. In early 2026, the rule is still popular among beginners who want structure without complex planning.

Key Takeaways On 50 30 20 Rule Of Investing

- 50 percent for needs

- 30 percent for wants

- 20 percent for savings and investments

- Still trending in 2026 among new investors

- Many people now adapt it due to rising living costs

The appeal of this method lies in its simplicity. It creates discipline without removing lifestyle comfort. People also like how it supports consistent progress toward future goals. Many banks, educators, and finance pages continue to promote it as an easy way to build financial stability.

Also Read: 10 5 3 Rule Of Investment: A Simple Guide For Realistic Returns

What Is The 50 30 20 Rule?

The 50 30 20 rule divides your after tax income into three categories. 50 percent goes to essential needs. 30 percent goes to wants. 20 percent is set aside for savings, investments, or debt repayment. This gives structure to spending and prevents mixing daily costs with long term planning.

Needs include rent, utilities, groceries, transport, healthcare, school fees, and other essential bills. Wants include entertainment, dining, shopping, gadgets, travel, and lifestyle extras. Savings include emergency funds, retirement planning, mutual funds, insurance, fixed deposits, or any long term investment.

This breakdown keeps daily life stable while helping money grow for the future.

Why People Continue To Follow The Rule

Many new investors and young professionals say the 50 30 20 framework feels balanced. It allows enjoyment without guilt. It also prevents lifestyle creep because needs are capped at half of income. People often set the 20 percent for savings on auto debit. This creates regular investing without effort.

Finance educators call it a healthy starting ratio. Beginners find it easy to understand and apply. Many users online describe it as simple to follow, even without deep financial knowledge.

Banks and financial institutions also continue to promote it in 2026. They highlight its role in improving money discipline and long term wealth creation.

Example Of The 50 30 20 Rule

Suppose your monthly income after tax is ₹ 1,00,000.

Here is how the income may be divided:

Needs (50 percent): ₹ 50,000

Wants (30 percent): ₹ 30,000

Savings and Investments (20 percent): ₹ 20,000

This structure helps you enjoy life today while still preparing for tomorrow.

How The Rule Supports Investing

The core strength of this model is the 20 percent investment share. This portion can go toward:

- emergency fund

- retirement planning

- mutual funds

- fixed deposits

- insurance linked savings plans

- long term equity investing

Even small, steady amounts can grow over time due to compounding. This helps reduce financial stress during emergencies and future life events.

Savings also reduce the chance of debt dependency.

Growing Public Interest And Online Trends In 2026

On X (formerly Twitter), discussion around the 50 30 20 rule remains active. Many people still praise the method as a clean way to structure income. It is often shared as financial advice during the start of the year when people reset money habits.

Several users describe how the rule prevents emotional spending. Others point out that it allows fun spending without guilt since wants already have a fixed place. The method is also presented by financial educators, banks, insurers, and investment pages as a tool for better financial hygiene.

Beginners online often call it easy to implement. Some refer to it as a balanced starting point for money management.

Listicle: Benefits Of The 50 30 20 Rule

- Encourages disciplined saving

- Keeps needs and wants clearly separated

- Reduces financial stress

- Supports long term wealth building

- Easy to apply without tools or advanced knowledge

Criticism And Evolving Views In 2026

At the same time, many posts online now question whether the classic 50 30 20 split fits current economic reality. Rising costs, inflation, and higher rent levels make it difficult for many households to keep needs under 50 percent.

Some people share that even basic living costs cross 60 to 70 percent of income. For them, the rule becomes hard to apply. Others argue that saving only 20 percent may feel slow for wealth creation in today’s market.

This has led to a wave of new variations. Some popular adjusted structures include:

40 20 40

50 40 10

60 20 20

80 20

These models often push for higher investment portions to speed up financial independence.

Several finance voices online say that more aggressive investing helps counter inflation and rising costs. Others encourage cutting lifestyle spending to increase future savings.

Still, many users agree that the rule should act as a guideline, not a strict rule.

How To Apply The Rule In Real Life

Start by calculating your monthly after tax income. Then list your expenses and group them into needs, wants, and savings. Compare your spending pattern with the recommended split. Adjust slowly if needed.

Automation helps maintain discipline. Setting up auto transfers for the 20 percent investment portion removes manual effort.

Tracking needs is equally important. This prevents overspending on lifestyle items.

Does The Rule Still Work For Investing Today?

The rule continues to hold value for beginners. It creates structure and encourages investing consistency. Over time, this habit can transform financial security.

However, it may need adjustment based on income level, city, cost of living, debt, family size, and goals. The main idea is to save and invest regularly. The exact ratio can be flexible.

Final Word

The 50 30 20 rule remains a strong starting framework in 2026. It keeps money organised into simple categories that anyone can follow. Public opinion shows both support and adaptation. Some follow it as it is. Others adjust it to handle higher savings or increased living costs.

What remains constant is the focus on discipline. A clear system helps people stay prepared for emergencies, goals, and long term security. Whether you choose 50 30 20 or a modified version, the habit of saving and investing remains the real key to financial progress.

Tags: 50 30 20 rule, budgeting tips, personal finance, investing basics, money management, savings plan

Related Posts :

Share This Post