10 5 3 Rule Of Investment: A Simple Guide For Realistic Returns

10 5 3 Rule Of Investment: A Simple Guide For Realistic Returns

The 10 5 3 rule of investment is one of the most popular guidelines used by investors to understand how money may grow over time in different asset classes.

It gives a simple way to set realistic expectations from equity, debt and savings. Many financial educators still use this rule today because it helps people avoid chasing high and risky short term returns.

Key Takeaways On 10 5 3 Rule

- The 10 5 3 rule gives a simple estimate of expected long term returns.

- Equity is linked with about 10 percent returns. Debt is linked with about 5 percent returns. Savings and deposits are linked with about 3 percent returns.

- It promotes diversification and balanced investing.

- It is a guideline. It is not a promise of fixed returns.

- It helps new investors think long term.

The rule is discussed often on social media and financial blogs. Many experts say it is a good starting point for beginners. It also helps remind people that higher returns generally involve higher risk. The idea is not new, but it continues to remain relevant for long term wealth building.

Table of Contents

Also Read: 50 30 20 Rule Of Investing

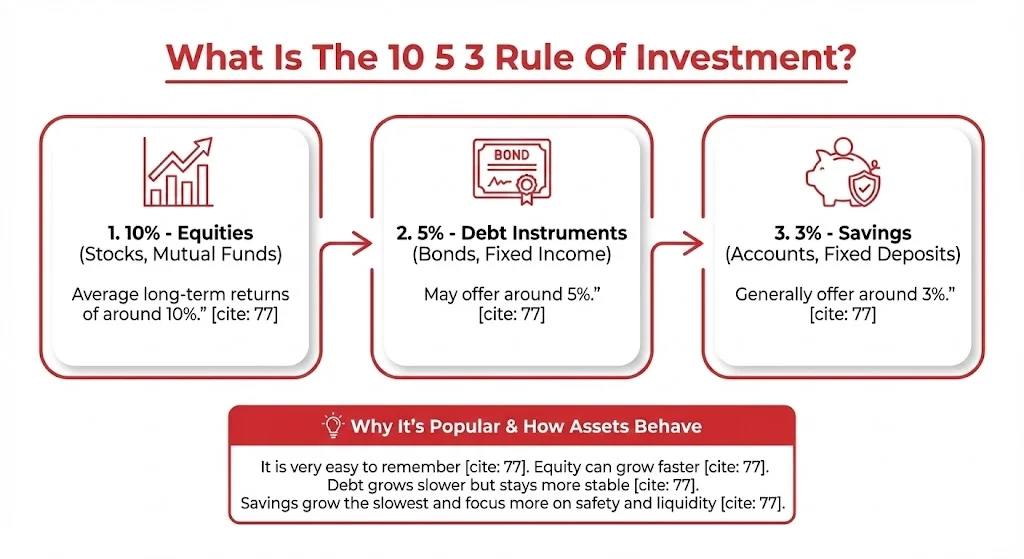

What Is The 10 5 3 Rule Of Investment

The 10 5 3 rule states that investors can expect average long term returns of around 10 percent from equities like stocks and mutual funds. Debt instruments like bonds and fixed income products may offer around 5 percent. Savings accounts and fixed deposits generally offer around 3 percent.

This rule became popular because it is very easy to remember. It also reflects how different assets behave over long periods. Equity can grow faster. Debt grows slower but stays more stable. Savings grow the slowest and focus more on safety and liquidity.

Why The Rule Matters For Investors

Many new investors enter the market with very high expectations. Some expect 15 to 20 percent returns every year. This is not always realistic. Markets move up and down. There are bull markets. There are also weak phases. The 10 5 3 rule reminds investors that returns average out over long periods.

It also highlights why equity plays an important role in wealth creation. If all money sits only in bank accounts, the growth is slow. Inflation can also reduce real value over time. So, the rule guides investors toward balanced allocation.

Public Interest And Recent Trends On X

This rule continues to trend across financial education communities. Many social media users refer to it as a golden thumb rule for investing. Educators share it while teaching beginners why investing beats saving over long periods.

For example, in late 2025, multiple users on X highlighted that stocks can be linked with around 10 percent returns. Debt instruments may earn around 5 percent. Savings may remain near 3 percent. Many posts also called it a simple way to build realistic expectations.

People appreciate that it promotes patience. It also helps reduce panic during market corrections. Some experts did state that returns may change based on market cycles. But the rule still works as a long term directional guide.

How The Rule Works In Practical Investing

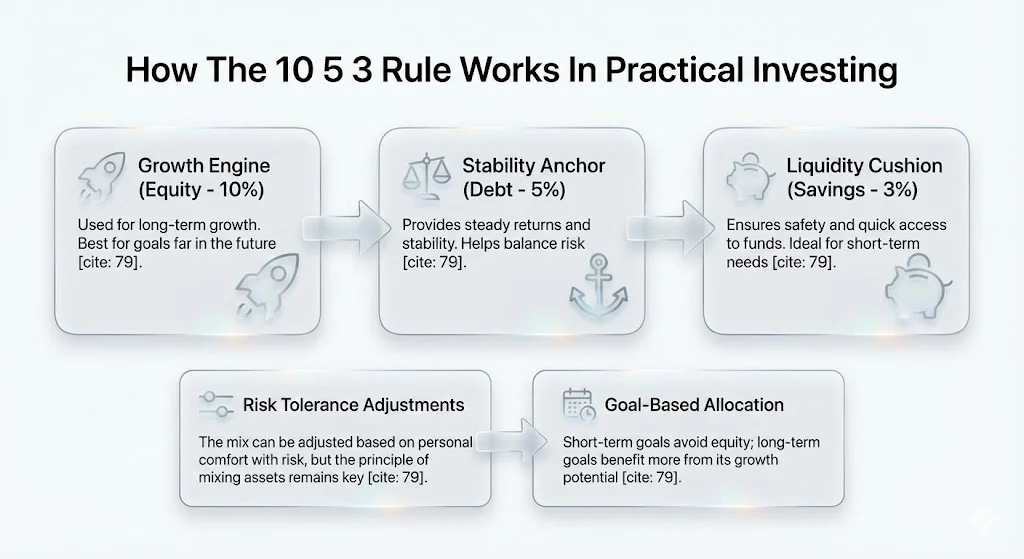

Investors can apply the 10 5 3 rule when planning their portfolio. Equity can be seen as the growth engine. Debt can help with stability. Savings can work as a liquidity cushion.

Different investors may have different risk tolerance levels. Some may choose more equity. Some may prefer more debt. But the idea of mixing assets remains useful across all profiles.

Your financial goals also matter. Short term goals usually do not suit equity. Long term goals benefit more from it.

The Logic Behind The Numbers

Equity carries higher risk. Prices move daily. But long term equity investments often reward investors with higher growth.

Debt products like bonds offer lower risk. So, returns usually remain moderate. Savings focus on safety and easy access. So, growth is usually the lowest.

This is the basic thought process behind the 10 5 3 structure.

Example Of Return Difference Over Time

Here is a simple listicle that shows how the same monthly investment may grow differently across asset types under the 10 5 3 guideline:

- Monthly Investment: Rs 10,000

- Time Period: 15 years

- Equity at 10 percent: Around Rs 38.6 lakh

- Debt at 5 percent: Around Rs 25.8 lakh

- Savings at 3 percent: Around Rs 22 lakh

This shows how asset choice matters over long horizons. Equity can help build a larger corpus. Savings keep money safe but grow slower.

Role Of Diversification

The 10 5 3 rule also reminds investors about diversification. Putting all money in one place increases risk. A mix of equity, debt and savings can protect wealth during market volatility. This balance can support both safety and growth.

Many Indian investors follow this mix through mutual funds, EPF, NPS and bank deposits.

Public Sentiment Toward The Rule

Recent social media posts showed strong support for this rule. People like how it simplifies financial planning. Many users say it helped them avoid unrealistic expectations. Others mention it prevents overdependence on bank deposits.

Some creators also include it in lists of important financial rules. These often appear with Rule of 72, 50 30 20 budgeting and other basic money concepts.

Things Investors Should Remember

Returns are not guaranteed. Equity returns can sometimes be lower than 10 percent, especially during weak cycles. At other times, they may be higher. Debt and savings rates also change with policy and economic conditions.

So, the 10 5 3 rule should be used as a framework. It should not be treated as an assured return plan.

Investors should also consider inflation and taxes. Real returns matter more than nominal figures.

Who Should Use This Rule

This rule suits beginners who want clarity. It also suits long term investors who want a basic benchmark. It helps in planning retirement, education funds and other future goals.

Financial advisors often use this rule during client education as well.

Why The Rule Remains Popular Today

Even in 2025 and 2026, experts continue to refer to the 10 5 3 rule. Some forecasts suggest equity returns may stay slightly lower in certain global markets. Still, the idea of relative difference between equity, debt and savings remains valid.

The rule supports disciplined investing. It keeps expectations grounded. It prevents short term chasing of high risk products. This is why it remains a key concept in financial literacy.

Final Word On 10 5 3 Rule

The 10 5 3 rule of investment is a simple but powerful guideline for everyday investors. It sets fair expectations from equity, debt and savings. It also shows why diversification matters. The rule is not a guarantee. It is a planning tool that encourages long term thinking.

Investors who follow structured asset allocation often build wealth more steadily. This rule helps them stay calm through market ups and downs and stay focused on their financial goals.

Also Read: The 5/25 Rule: A Simple Method For Ruthless Focus And Real ProgressThe 5/25 Rule: A Simple Method For Ruthless Focus And Real Progress

Tags: investment rules, 10 5 3 rule, personal finance, mutual funds, long term investing, wealth planning

Related Posts :

Share This Post